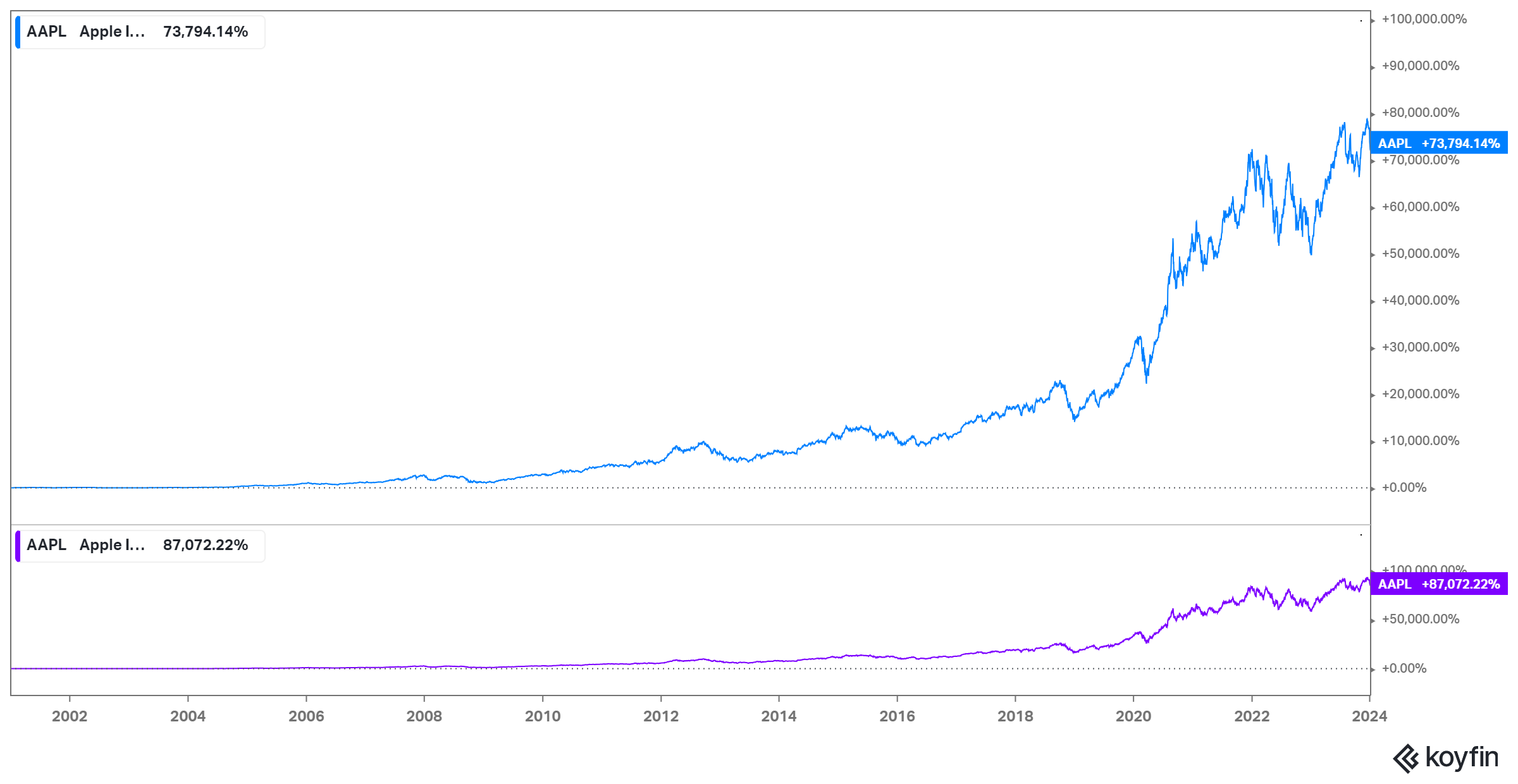

On December 22, 2000, shares of Apple Computer (the name was changed to Apple Inc. in early 2007) traded at $14.50 per share. Since then, Apple stock has gained just shy of 74,000%. Including dividends, a $1,000 investment in December 2000 would be worth more than $870,000 today.

source: Koyfin

Given those staggering returns, if an investor had recommended AAPL 23-plus years ago, he would certainly have some bragging rights. Over at Value Investors Club, an investor with the handle ‘paul62’ did just that. (VIC is a subscription platform, but articles older than six months can be viewed with a free membership.) At least in terms of returns, it is perhaps the best stock recommendation ever published online — and it’s a recommendation that provides interesting lessons about investing.

An Obvious Buy

In retrospect, AAPL in December 2000 looks like a no-brainer. Shares looked incredibly cheap looking backwards. Shares traded at less than 7x the company’s earnings for fiscal year 2000 (which ended September 30).

Even that didn’t tell the whole story: Apple also had just over $4 billion in cash and short-term investments, and just $300 million in debt. There was another $786 million in long-term investments in both debt and equity. As paul62 noted, those investments included stakes in Earthlink, Akamai Technologies AKAM 0.00%↑, Samsung, and ARM Holdings ARM 0.00%↑.

All told, net of debt Apple had about $4.5 billion in cash and investments. Incredibly, at the time, its market capitalization was just over $5.2 billion. Apple’s enterprise value was barely over $700 million, yet in fiscal 2000 it had earned $786 million in net profit. Adjusted for its liquid assets, then, Apple stock traded for less than one times earnings.

To be sure, the fundamentals weren’t quite that good. The $786 million in net profit did include a non-cash gain on sale from the company’s investment in ARM. But, after taxes, that gain represented just over one-third of reported net profit. On an operating basis, AAPL was well under 2x net earnings.

And it traded at that level not necessarily because of anything wrong with the business, but because of something very wrong with the market. The dot-com bubble1 peaked in March of 2000; by the end of the year the NASDAQ 100 had halved. (Quite famously, that index would not make new highs until 2014.) The crash affected Apple as a stock, and in the short term hurt Apple as a business. As paul62 noted, sharply slowing demand for computers (in part because many startups had so quickly gone bust) led to an inventory glut which the company would need to work through.

In Apple’s fourth quarter earnings release from October 2000, then chief executive officer Steve Jobs forecast a “second disappointing financial quarter” in Q1 FY01, due to elevated inventories at Apple’s direct customers. Even so, Apple still guided for revenue to be down only modestly for the full year, with expected earnings per share of $1.10-$1.25. At the low end, that still translated to roughly $400 million in net income — leaving AAPL still trading at less than 2x earnings.

Why Was AAPL So Cheap?

The obvious question looking backwards is: did investors lose their minds? Clearly, Apple in 2000 was not what Apple is today, but it was still a wonderful business. Again, the company generated over half a billion dollars in operating income in a single year.

But if you look more closely, there are some potential factors that could have given investors pause. The issue for Apple was not just the dot-com bubble. Ahead of the fiscal Q4 release in October, Apple gave a profit warning in which it said educational sales had disappointed, as had sales of the new Power Mac G4 Cube.

Both aspects of the guidance were concerning. The education market in theory should have been immune to the pressures in the corporate world. More importantly, education long had been Apple’s strength, but in 1999 Dell DELL 0.00%↑ passed Apple in terms of market share. Apple’s outlook for fiscal 2001 suggested market share losses might well be accelerating, particularly with the rise of other PC makers like Gateway and Compaq.

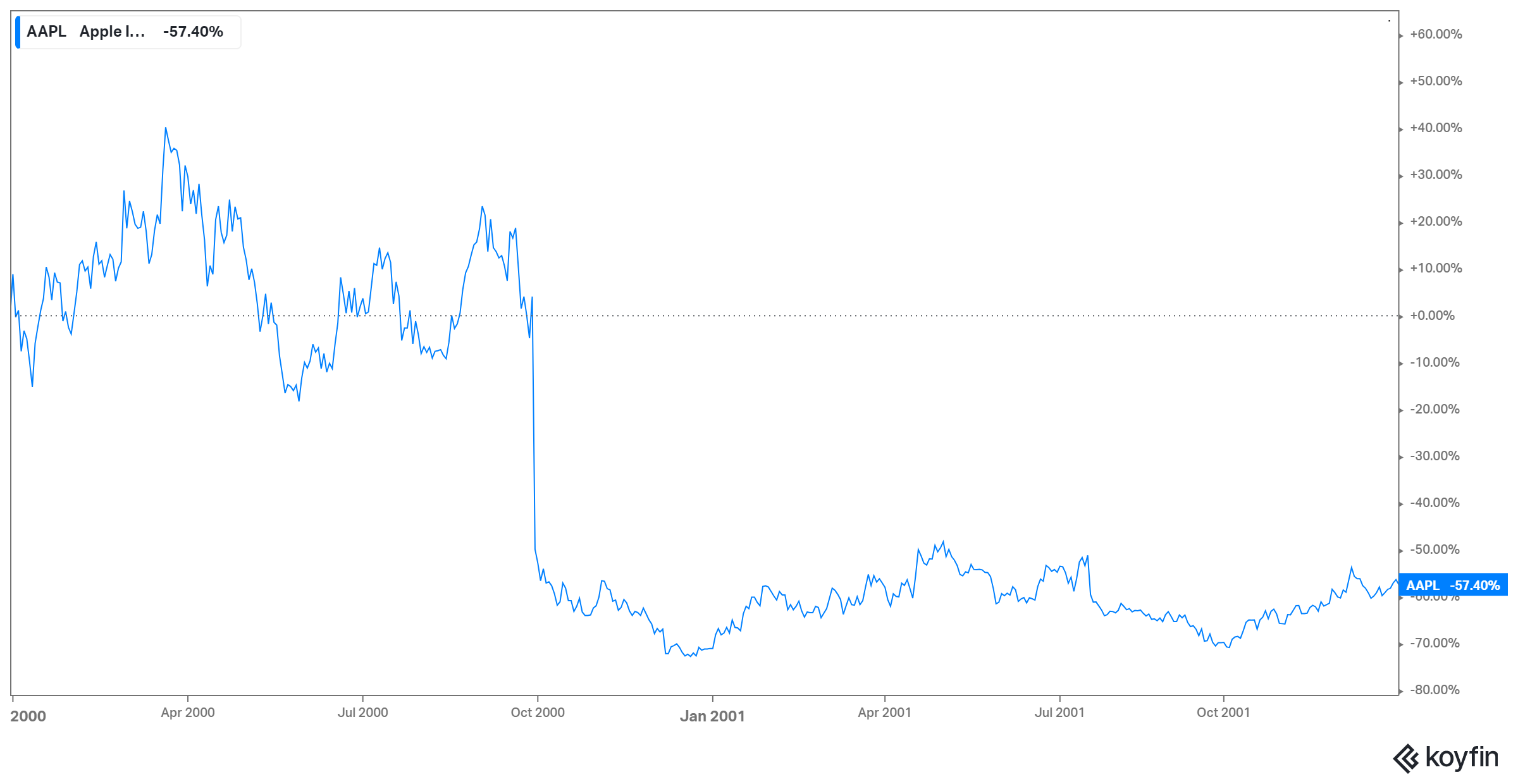

As for the Cube, Apple had launched the product only a couple of months earlier, at which point Jobs called it “simply the coolest computer ever”. A miss with that key product suggested several quarters of disappointing growth before the next major launch. Plus the possibility that Jobs’ ability to assess ‘cool’ wasn’t quite what investors thought it was. It was that September pre-announcement that really crushed AAPL stock, not necessarily the dot-com bust:

source: Koyfin

The long-term AAPL chart suggests that all worked out just fine. But in fact, it didn’t. The G4 Cube, which Apple pitched as an “entirely new class of computer”, was a cubic computer housed in acrylic glass:

source: Wikipedia

It was also, as current CEO Tim Cook termed it in 2017, a “spectacular failure”. The high-end model cost $2,299 (over $4,000 in 2024 dollars), yet without a clear end market the product didn’t sell. The Cube was discontinued after just one year. As for the updated guidance for fiscal 2001? Apple didn’t even come close. Actual sales were $5.36 billion, against the initial outlook of $7.5 billion to $8 billion. Apple didn’t generate $400 million in net income. It posted a net loss for the year (even with more help from investment sales).

A Lack Of Trust

In other words, from a short-term standpoint the market kind of had it right. And it’s important to put that perspective in the context of Apple’s longer-term story as of late 2000.

Bear in mind that Jobs had left Apple in 1985, returning 12 years later to the day. In the months before he came back, Apple was in serious financial trouble. It was, in fact, Microsoft MSFT 0.00%↑ that saved Apple2, with a $150 million preferred stock investment made weeks before Jobs came back.

From that point on, Apple’s financial results inflected positively. But, of course, it was impossible to know exactly why that had happened. Was it Jobs’s brilliance? Or the fact that the personal computer market was exploding, and a rising tide was lifting even the leaky Apple boat?

Some investors believed the latter. There are only four comments on the VIC piece, but they all get to various aspects of the bearish take on AAPL at the time. One provides its own lesson. The commenter writes that I would be a “buyer below 14”, which is an all-time case of being penny wise and pound foolish. At that valuation, a few percentage points in price simply didn’t warrant the risk of missing the opportunity. But even that bull writes that Apple “had better tech than some other companies [it] just marketed [its] products wrong.”

Another commenter snarkily gives Apple “credit for being able to be profitable long after their products have become irrelevant”. Further giving a sense of where Apple’s reputation actually was at the time, a third writes that “[I] would be more comfortable with an industry/sector leader such as Dell or Compaq [emphasis ours].“

In retrospect, however, the best is this one:

What troubles me is that when you ask the company about their plans for the large cash balance, the straightforward answer is that they plan to spend it on new initiatives.

One of those new initiatives was the iPod, launched in October 2001, a product that changed not just Apple’s fortunes, but (we’d argue) was the first step in the company’s transformation of global culture.

Lucky Or Good?

Given the comments, and even the somewhat muted nature of the recommendation itself — which focuses much more on the downside protection of the cash rather than the strength of the business — the recommendation of AAPL at a split-adjusted $0.259 per share seems to argue for contrarian investing. The market went one way; paul62 went the other, and wound up with positive returns.

But another way to look at is that AAPL in 2000 is simply a one-off, a massively lucky break. There was no way for paul62, or anyone else, to possibly forecast what Apple would become. At the time, no one knew that Apple would release the iPod, and when they did, this forum post from MacRumors shows massive (and, once again, hilarious in retrospect) disappointment from ardent Apple fans:

source: MacRumors

Certainly no one could have foreseen the iPhone. Research in Motion (now BlackBerry $BB) had gone public in 1997, and released its first device the following year, but that device was not actually a phone. As late as 2002, RIM’s stock was below $2. (It would peak at $147 in 2008.) Palm and other makers of PDAs (personal digital assistants) had seen their share prices plunge from March 2000 as well. The category at the time seemed something of a fad.

Meanwhile, in late 2000 the case for buying a busted tech stock near its cash balance (or below its cash balance) was in fact a great way to get into trouble, rather than to make profits. The market was littered with companies who had raised capital during the bubble but didn’t have profits, or any kind of real business model. No shortage of investors had bought those companies on the way down in August and October, seeing them as too cheap, only for those stocks to keep falling. Apple was certainly much better than nearly all of those companies, a good number of which eventually went bust, but, again, it had its own concerns and a hardly unblemished track record.

What Can We Learn From AAPL?

AAPL at a pre-split $14 looks in retrospect like an easy buy, but for many reasons it was not so at the time. But with the benefit of hindsight, there are some lessons the stock can impart.

The first echoes a theme we keep coming back to in this space: investing is hard. Concerns about Apple in 2000 were legitimate. The Mac business generated nearly $30 billion in sales during FY23. But there was absolutely a world in which Mac’s market share dwindled, and then created a vicious circle: software developers would devote their energies to PCs, making Macs less attractive by comparison, leading to more developer pressure, and so on.

Another lesson here is important: there are no perfect stories. It’s tempting to assume at first glance that AAPL was cheap in late 2000 because investors were panicked by the dot-com bust. Indeed, this leads to a common piece of investing advice: that good investors with a long-term focus just need to wait for the market to do something dumb (for lack of a better word) and capitalize.

But the market simply doesn’t do things that are that dumb that often. Again, there were legitimate company-specific concerns. AAPL had risks. Indeed, AAPL was a risk. All equity investments are. The market, then and now, rarely leaves profitable, growing companies with massive end markets trading for peanuts — even during one of the biggest sell-offs in modern history.

All that said, even ignoring the benefit of the hindsight, the risk/reward in AAPL in late 2000 was attractive, and there are lessons in that fact as well. The downside protection highlighted by paul62 was real, and important. The argument that Apple might blow its cash on “new initiatives”, as one commenter replied, ignored just how much cash the company had. It’s not just that cash and investments accounted for nearly 90% of the market cap, but that Jobs and his team couldn’t blow $4 billion even if they tried. In that context, AAPL was different than some busted IPO from 1999 — or, for that matter, 2024.

There’s also management. Steve Jobs in 2000 wasn’t the mythologized figure he became, but at the very least among Apple users he was immensely popular. Even before the iPod, let alone the iPhone, Jobs was an executive worth betting on. That, too, created a distinction from other cash-rich stocks with ugly charts. A good balance sheet is not enough; there needs to be a potential upside catalyst, and Jobs was one of those catalysts for AAPL.

That in turn gets to the lesson imparted by where AAPL headed over the next 23-plus years. By the end of 2001, the stock had gained 50%-plus from the lows. But even after that rally, the same bull case largely applied. Even with ugly FY01 financials, Apple with more than 60% of its market cap in liquid assets still would have been an excellent buy.

Apple stock closed 2002 slightly below where it was recommended here. But it then became clear that the iPod was a winner, and that iTunes would print cash, and that the Macintosh line had stabilized. By the end of 2004, AAPL had more than quadrupled from the lows — yet it still had more than one-quarter of its market cap in cash and investments and clearly had enormous growth opportunities from its new efforts.

By then, AAPL had a different bull case, and that case would go through various permutations over the next two decades. No doubt over that time some investors looked at the multi-year chart and thought the run was over, and sold their shares. Others believed that the opportunity for enormous upside had passed.

Quite obviously, it hadn’t. Since the end of 2004, AAPL still provided total returns of 16,000%. And that perhaps is the most important, and optimistic, lesson here: investors don’t have to bottom-tick the chart. The call by paul62 is about as good as it gets — but investors still had years left to make an awful lot of money.

As of this writing, Vince Martin has no positions in any securities mentioned.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

We’re using that term since it is so familiar, though as we’ve discussed elsewhere the bubble in telecommunications stocks was much larger.

Looking at Apple’s financials, and the fact that in 1997 the company paid $350 million in cash for NeXT, which Jobs founded after leaving Apple, the narrative that Microsoft “saved” Apple seems like it is probably overblown. But if so, it was a narrative that was overblown pretty much immediately, rather than one that was created later.