Editor’s Note: This is the sixth installment of our Fundamentals series, which aims to explain investing concepts. If you enjoy this series, let us know in the comments.

On November 30, 2006, the last day of fiscal year 2006, according to its annual report Lehman Brothers had total assets of $503.5 billion. The global investment bank also had $484.4 billion in liabilities, leaving stockholders’ equity (also known as book value) of $19.2 billion.

In other words, Lehman was levered about 26 to 1. The gross value of the assets ($503.5 billion) had a value roughly 26 times the net value of the assets ($503.5 billion less the $484.4 billion it owed) on its balance sheet. That multiple had soared over the previous five years. At the end of fiscal 2001, Lehman was less than eight times levered.

For a while, that increasing leverage was actually good news for Lehman Brothers and its shareholders. After an eight-month recession in 2001, Lehman had moved aggressively not just into mortgage-backed securities, but into originating the mortgages themselves. As housing prices soared during what only in retrospect was so clearly a bubble, so did Lehman’s assets and profits.

At the end of fiscal 2001 (ending November), Lehman had $64.7 billion in assets and book value of $8.4 billion. That year, the firm generated $1.16 billion in net income. Five years later, the asset base had increased eightfold and book value by about 130%. Net profits more than tripled.

Unsurprisingly, Lehman’s stock price responded to that growth. From 2002 to February 2007, shares roughly quadrupled. Less than two years later, in September 2008, Lehman filed for what is still the largest corporate bankruptcy in history. In less than a decade, the investment bank had shown both the promise and perils of leverage.

How Balance Sheet Leverage Works

To be sure, Lehman is an unusual example — and such a high-profile example that global banking regulators in the post-crisis period have made sure no financial institution can repeat Lehman’s experience. (Of course, Lehman was far from the only culprit.) Banks in general use leverage far more aggressively than do other kinds of companies. The very nature of fractional reserve banking requires leverage, though it does add risk to the system. That risk again came to the forefront earlier this year, when Silicon Valley Bank collapsed.

But most public companies outside the financial sector also use balance sheet leverage. As with banks, for these companies leverage increases risks and rewards, if not quite to the same level. To understand those risks and rewards, an overly simplistic example is useful.

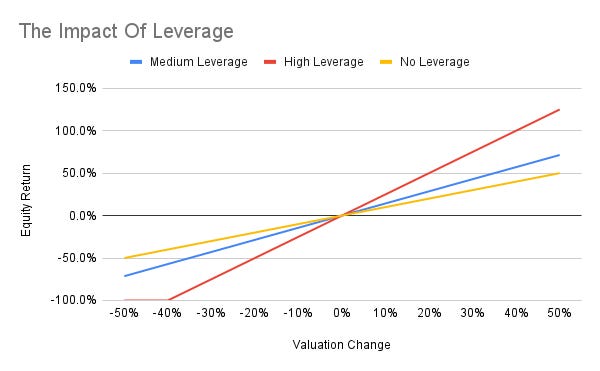

Imagine three businesses. Each business is worth $1 billion, but:

Company A has $300 million in debt (we’ll call it “medium leverage”);

Company B has $600 million in debt (“high leverage”);

Company C has no debt (“no leverage”).

For each business, we can split the $1 billion valuation into debt and equity. Company C has $1 billion in equity; despite the same valuation, Company B has just $400 million. For publicly traded companies, the $1 billion figure is known as enterprise value, the sum of its debt and equity; the total value of the equity is its market capitalization, which can also be calculated by multiplying the share price by the number of shares outstanding.

The medium-leverage Company A has a market cap of $700 million and debt of $300 million; Company B has a market cap of just $400 million and debt of $600 million; and Company C, since it has no debt has both a market cap and enterprise value of $1 billion. So what happens if we increase the overall valuation of each business by 10%, to $1.1 billion? The value of the equity increases at a quite different pace:

Company A (medium leverage): market cap climbs 14%, from $700 million to $800 million

Company B (high leverage): market cap climbs 25%, from $400 million to $500 million

Company C (no leverage): market cap climbs 10%, from $1 billion to $1.1 billion

The greater the balance sheet leverage, the higher the returns on the exact same increase in the valuation of the business. But, of course, the converse is true: if you cut the valuation of the business by 10%, the higher-leverage businesses underperform. In fact, at least on paper, if you reduce the valuation of each business by 40%, equity in the high-leverage business is completely wiped out.

In practice, this is not completely true1, but, again, this is a simplistic model. The broad point still holds: balance sheet debt amplifies both upside and downside. This is why that debt is referred to as leverage: it acts in much the same way as does a physical lever:

source: author

This is precisely why regulators have reacted to the financial crisis by removing the ability of systemic financial institutions from becoming so highly leveraged. When Lehman was levered 26 to 1, it took a roughly 4% decrease in its asset base to wipe out its entire book value. But even lower leverage can be dangerous.

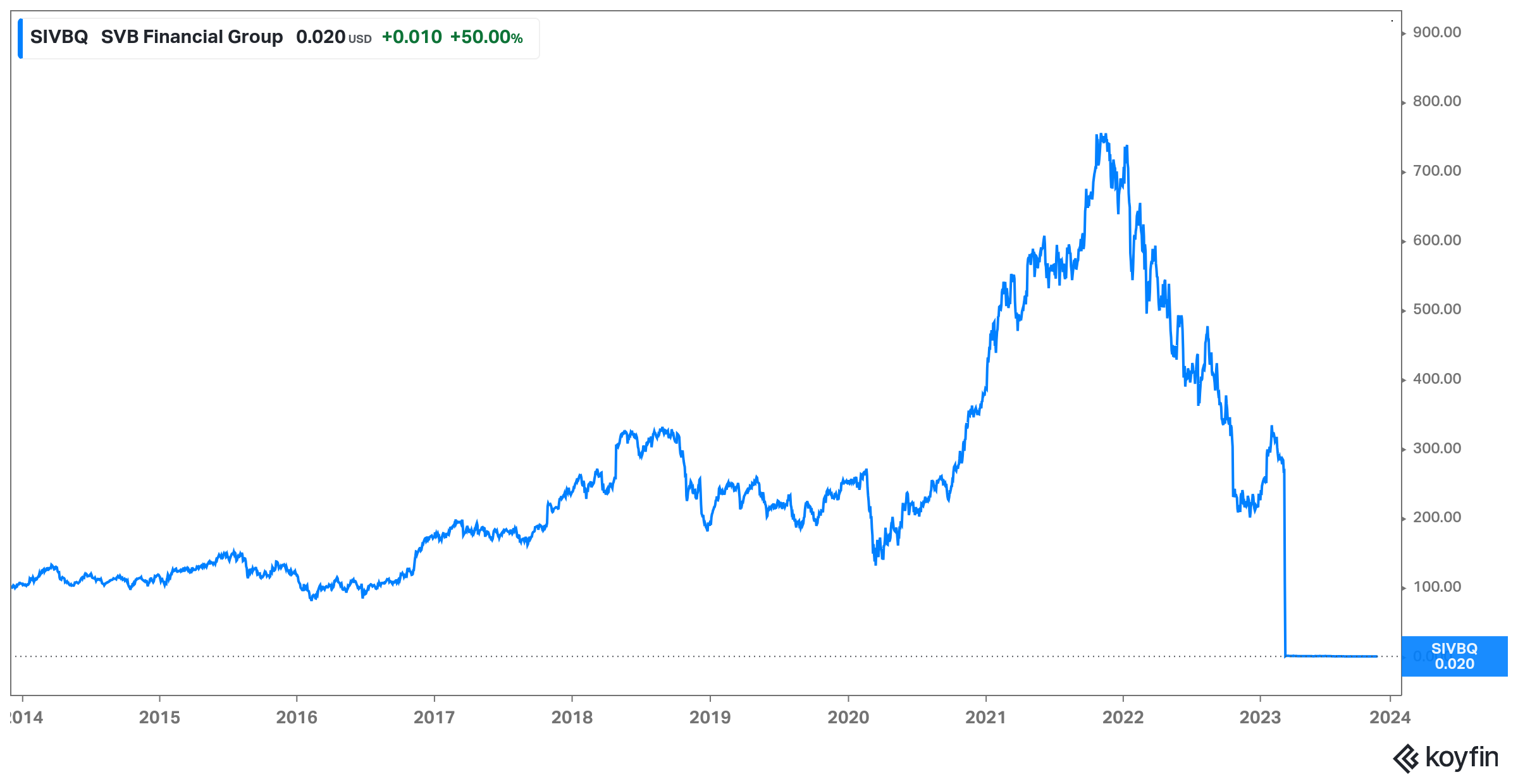

At the end of 2022, Silicon Valley Bank was about 13x levered, with total assets of $212 billion and net assets of just $16 billion. A relatively modest reduction in the value of the total asset base would wipe out those net assets, and leave the bank insolvent. That reduction — at least in the terms of the market value of the government bonds SVB held, if not the value at which they were carried on the balance sheet — came when the Federal Reserve quickly raised short-term interest rates, lowering the prices of long-term government bonds owned by the bank.

Investors began to realize that, when considering the market value of the company’s assets, the bank was technically insolvent. Customers soon followed the same logic, and after a classic “bank run” SVB collapsed2. Though the story was different from that of Lehman, the stock chart looked much the same. In early March 2023, SIVB stock had more than quadrupled over the previous decade; within weeks, the stock was zeroed.

source: Koyfin

The Impact of Debt On The Earnings Statement

Of course, debt isn’t free. Given those higher interest rates from the Federal Reserve, debt in fact is much more expensive than it was just a couple of years ago.

The interest paid on debt creates its own form of leverage. Corporate debt often has a fixed interest rate that does not change until the debt matures. Recent history aside, even interest on variable-rate debt3 generally leaves annual interest expense relatively stable.

The stability of interest expense contrasts with the potential variability (and hopefully growth) in the underlying business. And in this way, debt provides leverage on the profit and loss (or P&L) statement as well.

Let’s return to our three hypothetical companies. We’ll assume each business is generating operating income — also known as earnings before interest and taxes, or EBIT — of $100 million, can borrow money at 8%, and pays a 25% tax rate. The enterprise value to EBIT (EV/EBIT) multiple for each business is 10x, but because of interest expense, each company’s cash flows prove to be much different.

For Company A, its $300 million in debt creates $24 million in annual interest expense. With $100 million in EBIT, that leaves $76 million in pre-tax income, and $57 million in net (or after-tax) profit at the aforementioned 25% tax rate4.

Company B, with the highest debt level of $600 million, of course has the highest interest expense. At $48 million, it’s nearly half of operating income. Taxes take out another $13 million, leaving net profit of $39 million.

Company C, with no debt, simply is paying a 25% tax rate on its EBIT, leaving net profit of $75 million — nearly double that of Company B.

From this perspective, corporate debt seems, well, kind of dumb. Because of its debt, Company B’s net profit is barely half that of Company C — despite having an operating business that is (in this simplistic model) exactly the same.

But Company B’s equity holders actually are getting benefits in exchange for the lower free cash flow. The lower free cash flow is matched by a lower equity value. In fact, looking solely at net profit, the highest-leverage business, Company B, trades at a little over 10x net earnings ($400 million market cap, $39 million net profit); the zero-debt Company C trades at more than 13x ($1 billion market cap, $75 million).

As noted earlier, the leverage on the balance sheet magnifies upside from a valuation perspective if the business outperforms (as those equity holders believe it will; otherwise they wouldn’t own the equity in the first place). But there is also leverage in the P&L in which interest drives faster growth.

Assume each business grows its EBIT by 10%. The no-debt Company C grows net earnings 10%. Medium-debt Company A sees net profit rise to $64.5 million ($110 million in EBIT, $24 million in interest, $21.5 million in taxes), or growth of 13%. And heavily-leveraged Company B gets a huge jump: $7.5 million on a $39 million base, or an increase of more than 19%.

In other words, Company B does have a smaller equity value. But it also has a lower multiple relative to net earnings and faster bottom-line growth. To be sure, those lower multiples occur because the company is riskier: if operating profit starts to decline, the company’s net earnings will plunge at a faster rate. For shareholders who are bullish on the underlying business, however, that is obviously a risk worth taking.

Deleveraging: Where Debt Gets Really Interesting

If, overall, leverage increases returns and stocks on the whole go up, it would stand to reason that higher leverage overall would be a good thing. That’s not necessarily the case, however. Too much leverage can lead to a restructuring in a worst-case scenario — but it can also wreak havoc on an operating business even without a bankruptcy filing.

Employees can get nervous about the health of the business. Competitors can and will try and poach customers, arguing that they shouldn’t take the risk of a supplier going out of business. Management may be tempted to cut costs in a bid to cover interest expense, particularly during a recession. That’s precisely when cuts are most likely to lead to negative long-term consequences, such as the inability to retain talent or a failure to invest in opportunities that will drive growth when the external environment improves.

And there are businesses out there that have too much debt, even in the eyes of their own executives. Acquisitions can fail to provide the expected return — or simply require a debt load that the company plans to pay down with the additional cash flow from the purchased business. The sharp change in interest rates of late means that, for some companies, debt that was issued last decade, and maturing in the near future, will come with sharply higher interest rates as it is refinanced. And so for these companies, debt reduction, known as deleveraging, becomes a priority.

Deleveraging can be a significantly positive catalyst for a stock. That’s perhaps counterintuitive given the argument made above: that leverage can increase equity value and earnings growth. But, again, for companies for whom leverage has become not a modest amplifier of underlying growth, but a risk to that growth, reducing leverage can have significantly positive effects.

Let’s return to Company B, which had debt of $600 million, a market cap of $400 million, operating income of $100 million, and net earnings of $39 million. Management decides that the debt has become too unwieldy in a higher interest rate environment, and chooses to focus its efforts on reducing that debt.

In year 1, the company takes that $39 million in earnings5 and pays down debt. After 12 months, assuming the business has the same valuation and earnings power, the enterprise value should still be $1 billion. But now debt is just $561 million, and the equity ‘slice’, as it’s known, thus has expanded to $439 million. Simply by paying down debt, the value of Company B’s equity has risen by nearly 10% in a year.

Of course, there’s a virtuous circle effect as well. In Year 2, Company B’s has lower debt, and thus lower interest expense: 8% on $561 million is less than $45 million, again the previous $48 million. Earnings now increase by a little over $2 million after-tax; another $41 million in debt is repaid, adding 9% more in equity value simply by shrinking the debt portion of enterprise value.

This perhaps doesn’t sound like much. But this model is all occurring in a vacuum. If Company B can grow its operating income even modestly, thanks to leverage that will drive a strong increase in net income, which in turn means more debt reduction, which reduces interest expense, which means even higher net profit and free cash flow. And so the virtuous circle turns.

Any discussion of leverage, however, has to include the caveat that the virtuous circle can turn into a vicious cycle in an instant — and not just for financial institutions. Once interest is eating up a substantial portion of operating income — for Company B, nearly half in our simple model — the margin for error becomes exceedingly thin.

Any decrease in operating income means net income starts to decline at a rapid rate. Lower net income means that debt reduction is slower than hoped — or doesn’t happen at all. Equity investors get nervous, creditors get nervous, and suddenly the company is in a fight to access needed capital.

Leverage can turn sour exceptionally quickly. And it’s why investors are rightly cautious about overleveraged businesses. In theory, leverage can work wonderfully. Reality is often much trickier.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Even if the current estimated valuation of the business is less than debt, the equity still has some value, since there is a possibility that the current valuation can increase in the future. But for our purposes, the broad point highlights the downside risk: in a scenario where the valuation of the business drops 40%, the value of the equity will get crushed, even if losses aren’t quite 100%.

The story, of course, is not quite this simple.

Variable-rate debt usually has an interest rate calculated as a benchmark rate (often the Secured Overnight Financing Rate, which has mostly replaced LIBOR, the London Interbank Offered Rate) plus a spread. Sometimes the spread is fixed at, say, 400 basis points (four percentage points); sometimes the spread, too, is variable, depending on how much debt the company has outstanding relative to its earnings power.

For some heavily-indebted companies, there is a cap on how much interest is deducted, but, again, we’re using a simplistic model to get to a broad point.

We’ll assume that earnings in this case are equal to free cash flow.

"Company C has $1 billion in equity; despite the same valuation, Company A has just $400 million." Is that supposed to say company B in the second part of the sentence?

Great article! Are you familiar with AGS? Do you think a "beautiful deleveraging" is possible?