Research Notes: New Issues

Looking for value in the market's newest stocks — and then hoping for lower prices.

📍 TLDR

BLCO continues to tantalize, but execution needs to improve.

Sticking by HLN even after big gains, thanks to a key development on the legal front.

MBLY looks like a 2021-type rally in a 2022 market.

De-SPACs WEST and SYM look intriguing — at the right price.

It would seem that companies that went public in the last six months or so are either a) exceptionally desperate for cash (to be going public in such a volatile market) or b) exceptionally impressive companies, able to go public in such a volatile market.

There’s a bit of historical evidence to support that thesis. 2008-09 new issues included companies like Visa (to that point the largest IPO in history, executed in March 2008), Dollar General, and Hyatt, but also China-based frauds and battery developer A123 Systems, which would later go bankrupt1.

2022 has had a little bit of the same flavor. We haven’t quite got Chinese frauds (as far as we know), but as we covered in August there was some absolutely bonkers trading in a number of IPOs from China and Hong Kong. The highlight (or lowlight, depending on one’s perspective) was AMTD Digital which hit a peak market capitalization of $310 billion. (Yes, three hundred and ten billion U.S. dollars.)

There’s been some desperation, certainly. Controlled environment agriculture startup Edible Garden went public at $5 in May. The company has a decent chance of being bankrupt by year’s end. A couple dozen small-dollar offerings from June through August are down 60%-plus. That group includes an electric toothbrush manufacturer, an Israeli Amazon.com seller, a Malaysian e-commerce platform, and a California-based coffee chain with seven (seven!) locations.

There’s been some quality, too. Though certainly not to the level of Visa or Dollar General.

What makes the 2022 cohort of new stocks different, however, is the presence of SPACs (special purpose acquisition companies). That category is pretty much just desperation. Fast Radius closed its merger in February — and filed for bankruptcy last month. Quanergy Systems, a lidar developer, will shortly follow. Another nine de-SPACs that closed this year (thanks to SPACTrack.io for the data) are already down more than 95% from their merger prices.

If history does rhyme, there are some opportunities in the 2022 cohort — and maybe even in a de-SPAC or two. And so it’s worth taking a look at some of this year’s new stocks, in hope of finding those opportunities.

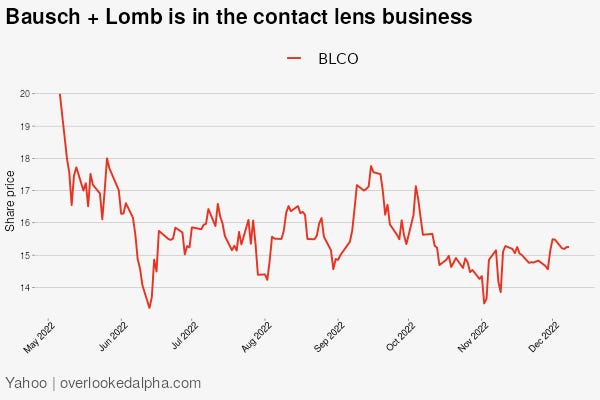

Bausch + Lomb

The contact lens business is underrated. It’s a four-company market with Bausch + Lomb BLCO 0.00%↑ , Alcon, Cooper Companies, and Johnson & Johnson. Profit margins are high, competition is rational, and there are tailwinds from developing markets (growth of the global middle class, better medical care, etc. etc.) and developed markets (increasing preference for disposables, which offer greater per-customer revenue and better margins).

And that’s why BLCO was tempting as part of Bausch Health (BHC), and why it's tempting after its May IPO. Investors are willing to pay up for these names, even with a few years of middling performance2. COO trades at about 17x this year's EBITDA; ALC 15x.

BLCO, meanwhile, based on post-Q3 guidance is barely above 10x. There are some differences between the businesses — Cooper gets about one-third of its revenue from a surgical business that focuses on women’s health — but not enough to explain the divergence in valuations. Investors simply don’t trust B+L.

For the most part, that skepticism has proven correct. B+L lost market share in recent years, and constant-currency growth in its Vision Care business has lagged year-to-date. Free cash flow has been soft, a problem for a company with a net leverage ratio past 3x.

And yet…the stock remains tempting here. It doesn’t take that much for the valuation gap to close. Organic growth remains positive. There’s room for margin expansion. Shares have been pretty much range-bound after an initial post-IPO sell-off, and there is a sense that if the business continues to lag, that’s probably the trend going forward as well. End markets are strong enough (even counting the roughly 38% of year-to-date revenue coming from surgical and pharmaceuticals) to keep profits at least afloat.

But if B+L can finally start taking some share, particularly in higher-margin disposables, there’s room for significant upside. A 2-turn expansion in the EBITDA multiple alone moves the stock up more than 25%. If that gain comes alongside market share stabilization, let alone growth, plus margin improvements, the upside is potentially significant over a multi-year period.

The overhang from Bausch Health (which still owns 89% of the company, and will need to sell more shares going forward) and continuing execution questions remain just enough to stay on the sidelines for now. But a cheaper price and/or improved results could change that quickly. BLCO remains on my personal watchlist, though admittedly it’s been there in some form for a few years now.

Mobileye

Mobileye MBLY 0.00%↑ is up about 50% since going public in late October. After that rally, it's not difficult to ask the question: are we really doing this again?

There’s value here, certainly. And if Mobileye really becomes a critical part of the autonomous vehicle industry, there’s probably upside long-term. ADAS (advanced driver-assistance system) sales can generate growth along the way.

But Mobileye is guiding for revenue to increase about 37% this year. GAAP gross margins YTD are under 50%. And the stock is trading (based on guidance) at more than 13x this year’s sales.

There are thin float dynamics at play here. The market has been more optimistic toward chip names in recent weeks, and in context Mobileye might look cheap: the current ~$25 billion market cap is about half of the valuation underwriters were floating back in April.

Even with those considerations, however, MBLY looks like a concerning piece of evidence that the market hasn’t quite learned the lessons imparted over the last eight months. Valuation matters. Investors need to consider gross margins when assigning price-to-revenue multiples (as we argued in one of our first posts, on CPaaS stocks). The future always comes slower than optimists suggest.

This really looks like a 2021-type rally. Again, maybe that’s just the result of a thin float, but maybe it’s a piece of evidence that the market is still hoping it’s found a bottom — which almost always means it hasn’t.

Westrock Coffee Company

As noted above, 11 of the 94 SPAC mergers that have closed this year are down 95%-plus. What makes that figure all the more incredible is that only eight are positive at all.

Westrock Coffee Company WEST 0.00%↑ is one of them. In fact, the stock touched an all-time high on Wednesday (at $14-plus, but still). Westrock is a coffee and tea manufacturer providing finished goods along with flavors and extracts, but with a focus on sustainability (including a platform for tracing coffee back to its source).

Unlike too many de-SPACs, this is a real business. It’s a significant supplier to major U.S. chains, claiming number one market share. Westrock’s extracts business should benefit from the growing preference for coffee drinks (notably, iced coffee) versus traditional brewed options. Coffee has been a pretty good business over time and Westrock has established a solid niche.

The one catch at the moment is, that like too many de-SPACs, Westrock has already disappointed against its expectations. As recently as June, for 2022 the company was projecting $960 million in revenue and $75 million in Adjusted EBITDA. Guidance given post-Q3 is for $850-$890 million in sales, and $60-$63 million in EBITDA.

WEST has powered through that report, but after the rally it’s a bit more difficult to pound the table for the stock, at nearly 20x this year’s EBITDA (and with implied margins of ~7%). But we’ve seen de-SPACs like this reverse violently a few months after merger close. Fellow coffee play BRC is a good example, though that right-wing-ish business had some meme characteristics). If WEST sees a reversal, a mid-teens EBITDA multiple does seem reasonable.

Symbotic

Symbotic SYM 0.00%↑ sounds like one of the many ridiculous de-SPACs we've seen over the past two years. Here's how the company describes itself:

Symbotic is an automation technology leader reimagining the supply chain with its end-to-end, A.I.-powered robotic and software platform. Symbotic reinvents the warehouse as a strategic asset for the world’s largest retail, wholesale, and food & beverage companies.

It sounds a little pumpy, to put it mildly, and perfect for the core attribute of the de-SPAC transaction versus the IPO: the ability to make out-year projections.

But this, too, is a real business. Fiscal 2022 (ending September) revenue was $593 million. The figure increased 167% in Q4, and Symbotic is guiding for 100%-plus growth in Q1 FY23. Customers include Albertsons and Walmart, the latter of which also invested in the company alongside the merger.

There are concerns here, of course. The Symbotic system is a massive installation, so sales cycles are going to be long and revenue likely a bit lumpy. Adjusted EBITDA margins remain sharply negative, in part because gross margins are low (just 17% in FY22).

But it’s worth noting that Symbotic beat its original top-line outlook for FY22. When the merger was announced in December (two-plus months into the year), the company guided for revenue of $436 million. Gross profit dollars did miss, a potential red flag; margins were guided to 23% instead of the actual 17%. That in turn led to disappointment in Adjusted EBITDA, with -$90M actual against a guided -$38M.

Still, the balance sheet is strong enough ($350M+ in cash) that delayed profitability doesn’t cause solvency risk. There would seem to be mid-term tailwinds from tight labor markets post-COVID and resulting intense demand for automation.

The catch — and it’s a big one — is valuation. Fully-diluted market cap nears $6 billion3. That's 60x trailing twelve-month gross profit. Given growth, that multiple is going to narrow in a hurry, but back of the envelope, even a nearly $1 billion revenue print in FY23 still may not support that kind of valuation. But if SYM takes a tumble (and in this market, it absolutely can) there's an intriguing, and even somewhat defensive, story on offer.

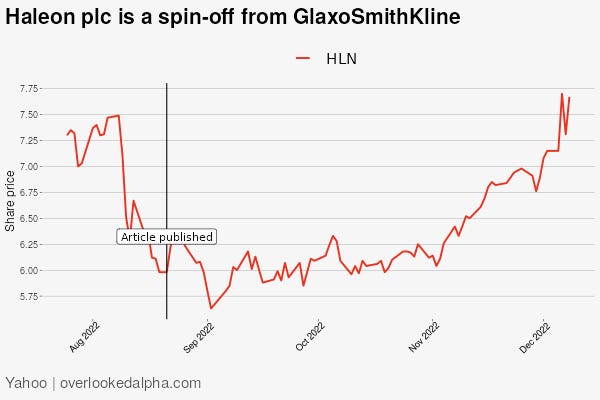

Haleon

We’re wedging Haleon HLN 0.00%↑ in here a bit, as it wasn’t an IPO, but rather the year’s biggest spin-off. The manufacturer of over-the-counter medications was separated from GSK in July, and HLN stock promptly fell to under $6 a share:

That kind of decline isn’t unusual for spin-offs, as the transaction can lead to “forced selling” by index funds and institutional investors if the SpinCo no longer satisfies their mandates. But as we wrote in recommending HLN in mid-August, the delayed nature of the selling suggested another possible cause.

In early August, HLN, GSK, and Sanofi SA were all hit by significant sell-offs. The issue appeared to be potential exposure to lawsuits over the antacid Zantac (ranitidine). All told, the concerns created a $40 billion-plus hit to market capitalizations across several stocks.

We wrote at the time that the selling was confusing at best. Haleon had disclosed the risk in its F-1 ahead of the spin (see p.55). But in retrospect, it appears that Zantac lawsuits were indeed the cause. HLN rallied 7% in a red market on Tuesday (GSK and SNY were +8%) after a federal judge tossed the lawsuit.

Those gains continued a rally following a solid third quarter report last month. Haleon raised full-year revenue guidance displaying a strong ability to manage an inflationary environment. Yet the stock still is trading at ~18x this year’s earnings (pro forma for higher post-spin interest expense). For this combination of growth and defensiveness that multiple remains attractive. Meanwhile, the rally on Tuesday only reverses a portion of the August decline that made no sense at the time.

HLN has rallied 29% since our call; we’re sticking by that call and HLN remains a solid position in my personal portfolio.

As of this writing, Vince Martin is long HLN.

Tickers mentioned: ACI 0.00%↑, ALC 0.00%↑, AMTD 0.00%↑, BHC 0.00%↑, BLCO 0.00%↑, BRCC 0.00%↑, COO 0.00%↑, DG 0.00%↑, EDBL 0.00%↑, FSR 0.00%↑, GSK 0.00%↑, H 0.00%↑, HLN 0.00%↑, JNJ 0.00%↑, MBLY 0.00%↑, QNGY 0.00%↑, SNY 0.00%↑, V 0.00%↑, WEST 0.00%↑, WMT 0.00%↑

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Notably, A123’s implosion led to the end of Fisker Automotive, the first attempt from Fisker Inc. FSR 0.00%↑ founder Henrik Fisker.

Since the April 9, 2019 spin-off of Alcon from Novartis NVS 0.00%↑, ALC is +17% and COO +9%. The S&P 500 has rallied 37% over the same stretch.

Some public sources show a much lower figure, but they don’t account for Class V-1 and Class V-3 stock)

By any chance , do you have any additional material on mobileye or can guide me somewhere. Would love to learn a bit more about it but in a layman terms