2023: The Year That Defied Expectations

We take a look back at the last 12 months

What stands out about 2023 is how thoroughly it defied expectations. Despite the most aggressive hiking cycle in history, U.S. equities posted a strong year. At Wednesday’s close, the S&P 500 is up 24.5% year-to-date; the Russell 2000 (thanks to a strong closing burst) 17.3%; and the NASDAQ 100 an incredible 54.4%. That figure is the best since 19991, better than the 53.5% generated in 2009.

Beyond major indices, the sense of surprise still holds. Higher interest rates were supposed to pressure not just the equity market as a whole, but housing plays in particular — yet homebuilders have been the best performers of the year. The only better group might be cryptocurrency miners2, another sector which in theory should have taken a hit from higher rates3. Meanwhile, healthcare stocks seemed set for a rally, amid a potential flight to defensive name. They’ve had their largest underperformance in three decades.

Perhaps the biggest surprise is just how unusual this market was. Coming into the year, the core expectation was probably for a return to normalcy. After all, following the novel coronavirus pandemic, that was the sense for life as a whole. (Though sadly global conflict also seems to have normalized).

Yet this was a year that saw massive trends hit — at least three of them. The fact that all three hit this year seems to be largely coincidental, but their sum effect was to create yet another year in which external factors significantly moved the market.

Regional Banks

There’s an interesting argument that the regional bank crisis that peaked when Silicon Valley Bank collapsed in March wasn’t really a crisis at all. The failure of SVB (and to a lesser extent the four banks that met the same fate later on) generated no shortage of commentary. Yet, nine months later, there’s little evidence that SVB mattered much to the broader financial system. The venture capital ecosystem that was supposedly being fed by the bank appears fine. The same is true for the U.S. economy, and of course for U.S. equities.

Even within the banking sector, the biggest predictions have not played out. There was a real sense that the biggest U.S. banks would be massive beneficiaries of the crisis, as depositors would flee toward the ‘safest’ institutions. That hasn’t happened.

In fact, right after SVB’s collapse, Roundhill Investments launched a Big Bank ETF (ticker BIGB), which at launch included equal-weight positions in the six largest U.S. financial institutions4. BIGB was designed specifically in response to the regional bank crisis, as a way to play the trend of deposits flowing to the largest banks. Roundhill closed the fund this month after gains of 12.5% — which actually lagged the S&P 500 over that period, and badly underperformed KRE (up about 44%).

There seems to be a pretty solid argument that the banking crisis not only is in the past, but in fact didn’t really matter. Even regional bank stocks themselves have bounced back: the SPDR S&P Regional Banking ETF KRE 0.00%↑ is up 18% just in the last month.

source: Koyfin

Yet fears that dominated the sector in March can’t be completely ignored. After all, the reason regional bank stocks have soared in recent weeks is because of the shift in the Federal Reserve’s posture.

Lower rates reduce the losses of long-dated securities that led to some of the worries about bank health at the beginning of the year. But those worries weren’t, and aren’t, really about whether banks were ‘technically insolvent’ on a mark-to-market basis, because that didn’t really matter5. What mattered, as SVB learned, is whether being ‘technically insolvent’ (or close) spooked depositors.

So if lower rates help regional banks, it’s because a) lower rates improve bank balance sheets in a way that should comfort depositors and/or b) lower rates decrease competition from higher-yield alternatives (including those offered by non-bank financial players like SoFi SOFI 0.00%↑ or even Robinhood HOOD 0.00%↑). But a year ago, investors weren’t worried about either of those factors.

Indeed, the fact that SVB (among others) was ‘insolvent’ on a mark-to-market basis was known by analysts and investors in the space. The bank’s bond portfolio was seen as a multi-year, if temporary, headwind to earnings that would eventually resolve itself as lower-yield bonds matured.

What many people underestimated was how depositors would react once presented with that fact. Those depositors proved to be much less loyal than investors (and regional bank executives) had believed. Assuming that holds in the future, regional banks will be at greater risk the next time uncertainty arises — and in banking, uncertainty always returns eventually.

Ozempic Changes The Market; Will It Change The World?

For the other two major trends of 2023, there is much less argument about whether they matter long-term. The precise impact of Ozempic and GLP-1 agonists is up for debate (we took a close look at that debate back in October). But there’s clearly something here, even if scientists did not accidentally invent an anti-addiction drug.

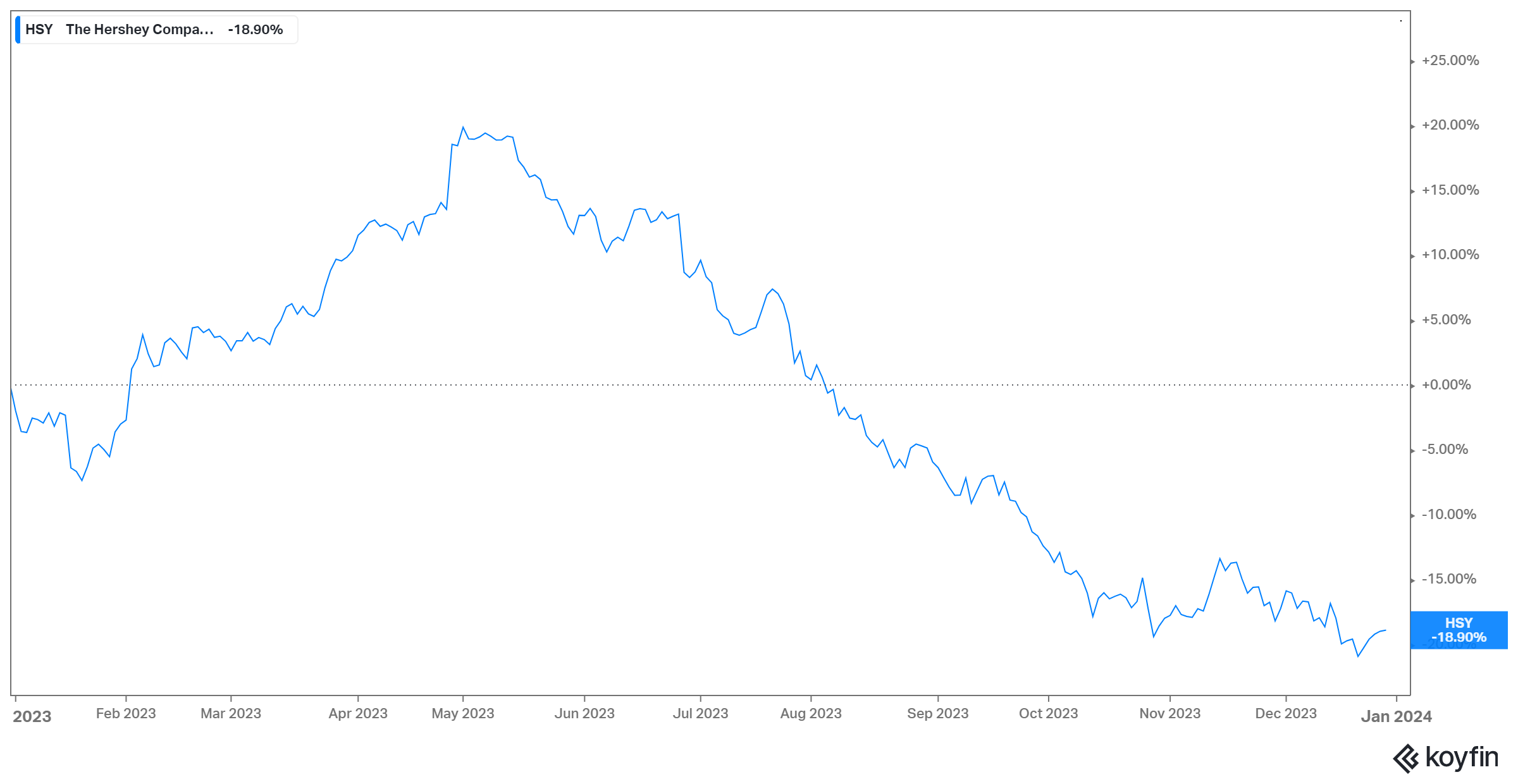

One thing that’s difficult to tell about Ozempic, is whether it’s responsible for falling stock prices in seemingly affected stocks. For instance, Hershey HSY 0.00%↑ seems the most obvious and most logical Ozempic victim. The stock peaked on May 1, about five weeks before Google searches for the term did the same. Since then, HSY has gone straight down:

source: Koyfin

But there are other reasons for the decline. Cocoa prices have soared. Inflation has led to some pushback: Hershey’s volume actually declined year-over-year in Q3. And HSY came into the year as an expensive play: shares traded for about 26x the consensus estimate for 2023 earnings per share.

Meanwhile, fellow candy play Mondelez MDLZ 0.00%↑ is actually up 8.4% so far this year. That’s a return that lags the broad market, but it comes after a solid 2022. Since the start of last year, MDLZ has actually crushed the S&P 500 (total returns of 14.1% versus just 3.5% for the S&P).

Demand for the drugs themselves certainly seems straightforward: Eli Lilly LLY 0.00%↑ and Novo Nordisk NVO 0.00%↑ have added well past $200 billion in market capitalization combined since the start of the year. But the secondary effects still seem somewhat muddled — which means the ‘Ozempic trade’, if it exists, is probably closer to the beginning than the end.

Artificial Intelligence And The Magnificent 7

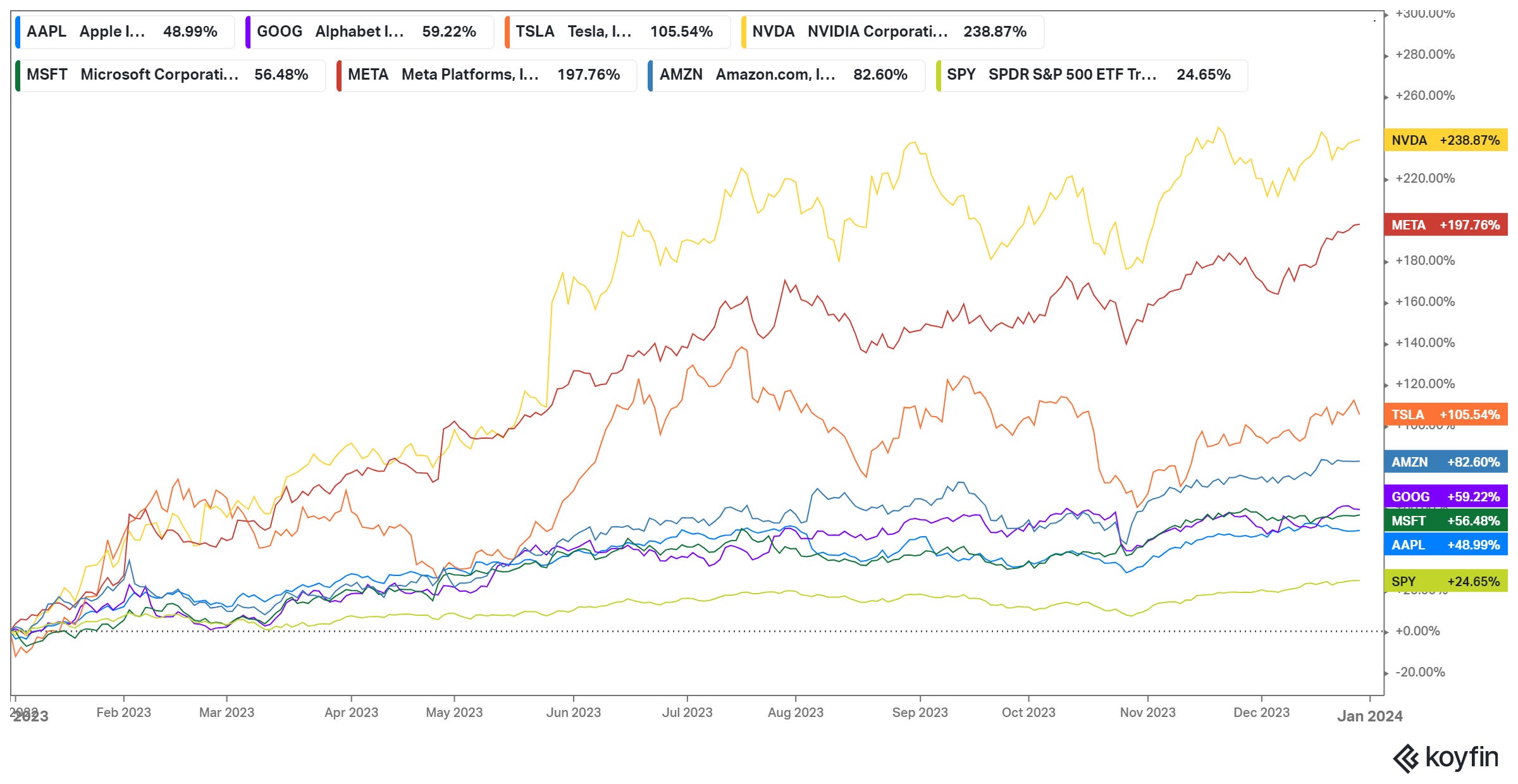

In naming Nvidia NVDA 0.00%↑ as our most impressive stock of 2023 last week, we noted the company’s role in making artificial intelligence a permanent, significant, part of the investing landscape. Nothing better proves that than the performance of the market’s most valuable companies.

As noted above, the S&P 500 is up 24% year-to-date. Nearly two-thirds of that rise has been created by just seven stocks, named the “Magnificent Seven” by BofA analyst Michael Hartnett.

source: Koyfin

The importance of these seven names6 to broad market returns has been widely reported. What seems less covered is the sheer size of the gains. Incredibly, each of Apple, Microsoft, and Nvidia has added just shy of $1 trillion in market cap this year alone. The total increase in equity value for the seven companies is now over $5 trillion.

Put another way, investors now project the discounted cash flows of these seven companies will be $5 trillion-plus higher than believed just twelve months ago. That in turn means an incremental $100 billion-plus annually just a few years from now7, with the figure growing from there. And that creates an interesting framework for thinking through the broader applications of artificial intelligence on the other 58,000 or so public companies worldwide.

The question is: where is that money coming from? The optimistic answer is that AI will raise global productivity. In that scenario, the Magnificent Seven will gain just a piece of the broader societal benefits they create.

The less optimistic answer for those that are not shareholders of the Magnificent 7 is that the market is signaling that, in an AI-driven world, the rich get richer. It will be incredibly difficult, if not outright impossible, for any company to compete with the technical resources, skilled workforce, and cost of capital of these behemoths. Most of the AI startups will fail (that’s the nature of that beast in general, and particularly in this type of industry); those that show early promise may well be acquired or at least heavily influenced by these giants (see, for instance, the relationship between Microsoft and OpenAI).

And the third answer is that the $5 trillion-plus figure is simply wrong. Hartnett himself has compared the seven to the “Four Horsemen” of the 1990s: Cisco, Dell, Intel and Microsoft. The seemingly unstoppable gains in those four names ended in a hurry.

In June we noted the almost eerie similarities between Nvidia then and Cisco at its early 2000 top. And we noted that what brought down Cisco was not just investors selling Cisco stock amid the bursting of the dot-com bubble. Rather, the biggest issue was that Cisco’s growth stopped — because its growth and that bubble were directly correlated.

Companies all of kinds moved into the online world, whether customers were ready or not, whether the offerings added value or not. And it was Cisco hardware that underpinned so many of those efforts. So when those online efforts were paused, or simply ended, Cisco’s demand flatlined.

We wrote earlier this year that Nvidia’s key risk was similar: that an early rush into AI would evolve into a more measured trot, leading to inventory buildups, hugely difficult year-prior comparisons, and thus the end of sizzling, or even any, top-line growth. At this point, however, that risk seems to apply to pretty much all of the Magnificent Seven. We have been here before: investors always assume the major trend will catch on more quickly than it does.

But there are frictions, and conflicts of interest (are employees going to move that aggressively toward helping to build technologies that will eventually displace them?), and bureaucracy and risk aversion among managers. In other words, all of the possible explanations for the AI-driven portion of gains in the Magnificent 7 could be correct. AI will raise productivity; it will hurt some portion of the population; and it will accrue even more profit to the world’s biggest companies. After such a spectacular rally, however, what matters is not just how AI proves to play out, but when.

As of this writing, Vince Martin is long SCHW.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

The index more than doubled that year, after increasing 85% the year before.

Among more than 3,500 stocks with a market capitalization of $300 million or higher, crypto miners are the 6th, 7th, 8th, 9th, and 12th-best performers.

The argument is that cryptocurrency prices should benefit from lower interest rates, but given crypto’s relative history that argument is still somewhat theoretical, and quite obviously did not play out in 2023.

Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo.

We discussed this at length in our recommendation of Charles Schwab, but the problem with long-dated bond portfolios was not the actual market value, but the hit to net interest margin caused by having to pay higher rates to depositors without corresponding increases in assets. As long as that hit was manageable (as in the case of SCHW), the problem was one of profitability, not solvency — barring a run on the bank.

Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta Platforms, and Tesla.

Presumably, AI will actually depress near-term profits for the group, even with Nvidia printing cash, due to heavy investments required to build AI capabilities and applications.