The most basic, and most familiar, form of yield comes from a savings account. A customer deposits $1,000 in an account that yields 3%, and every year she receives $30 in interest (usually paid monthly) while her $1,000 in principal remains untouched. It’s a simple, and essentially risk-free1, structure.

The simplicity of yield in banking accounts is, for the most part, an exceptionally good thing. The ability of depositors to move money with the click of a mouse did cause some problems during the regional banking crisis in March, as depositors fled banks with perceived risk. But from the perspective of those depositors, and the economy as a whole, it’s useful that individual customers (or indeed, small businesses) don’t need to evaluate the credit profile of their banks. Money goes in the bank, and that same money, plus a little bit extra, comes out on demand. Every single time.

But this simple structure creates problems as depositors move into investments that are more complex and less certain. Those investments do not act like bank accounts — and many investors get in trouble for assuming otherwise.

Dividend Yield Is Different Yield

Some stocks offer dividends, cash payouts that in the U.S. usually are paid quarterly at a consistent level that is meant to rise over time2. Those dividends thus look an awful lot like interest payments.

As a result, some investors take the framework of a savings account and apply it to equities: the amount invested is like the principal placed into an account, and the dividend yield — the annual amount of the dividend paid, divided by the current stock price — is just like interest.

So an investor might look at an online savings account from, say, SoFi SOFI 0.00%↑, and see a yield of 4.60%. And then, seemingly reasonably, she might look at AT&T T 0.00%↑ and see a dividend yield of 6.73%. AT&T’s yield is higher, and thus in this framework AT&T stock seems preferable as an investment meant to generate income.

Indeed, it’s common to see precisely this argument being made on social media or in the comment sections of investment websites. But shifting the framework of bank accounts to equity investments is wrong — and wrong twice.

The problem is that in a bank account, the principal is guaranteed. The interest rate is variable (it’s sensitive to broader interest rates as determined by the Federal Reserve), but some level of interest is guaranteed. In stocks, neither is the case.

A dividend is not interest. It’s not a contractual agreement, but rather paid solely at the option of a company’s board of directors. Ideally, that dividend rises over time. The likes of Procter & Gamble PG 0.00%↑ and Johnson & Johnson JNJ 0.00%↑ are so-called “Dividend Kings”, having not just paid, but increased, their dividends for 50 consecutive years or more. But there is no guarantee that any income investment (or any investment at all) is going to be as successful as those two giants have been.

Companies can cut or even eliminate their dividend at their discretion. Coming into this year, HanesBrands HBI 0.00%↑ had paid a dividend for nearly a decade; the company eliminated its payout in February. In May, Big Lots BIG 0.00%↑, stopped its program, which had begun in 2014. Cuts are more common: VF Corporation VFC 0.00%↑ came into this year as a Dividend King, and has since cut its dividend twice.

Stock Is Not Principal

The bigger issue, however, is that, unlike in a bank account, in an equity investment the principal is not guaranteed. The worst-case scenario for a bank account is that the interest rate drops back to near-zero and the accountholder is left with her initial deposit plus some interest. The worst-case scenario for the owner of a dividend stock is that the dividend is canceled and the stock goes to zero.

What is particularly dangerous about chasing high dividend stocks is that there’s a brutal “double whammy” effect: the dividend is cut because the business is performing poorly, which means the value of the initial investment plunges as well. As we noted last month, VFC is down 83% from its highs. BIG hit a 32-year low this year, and is off 90% from its 2021 peak.

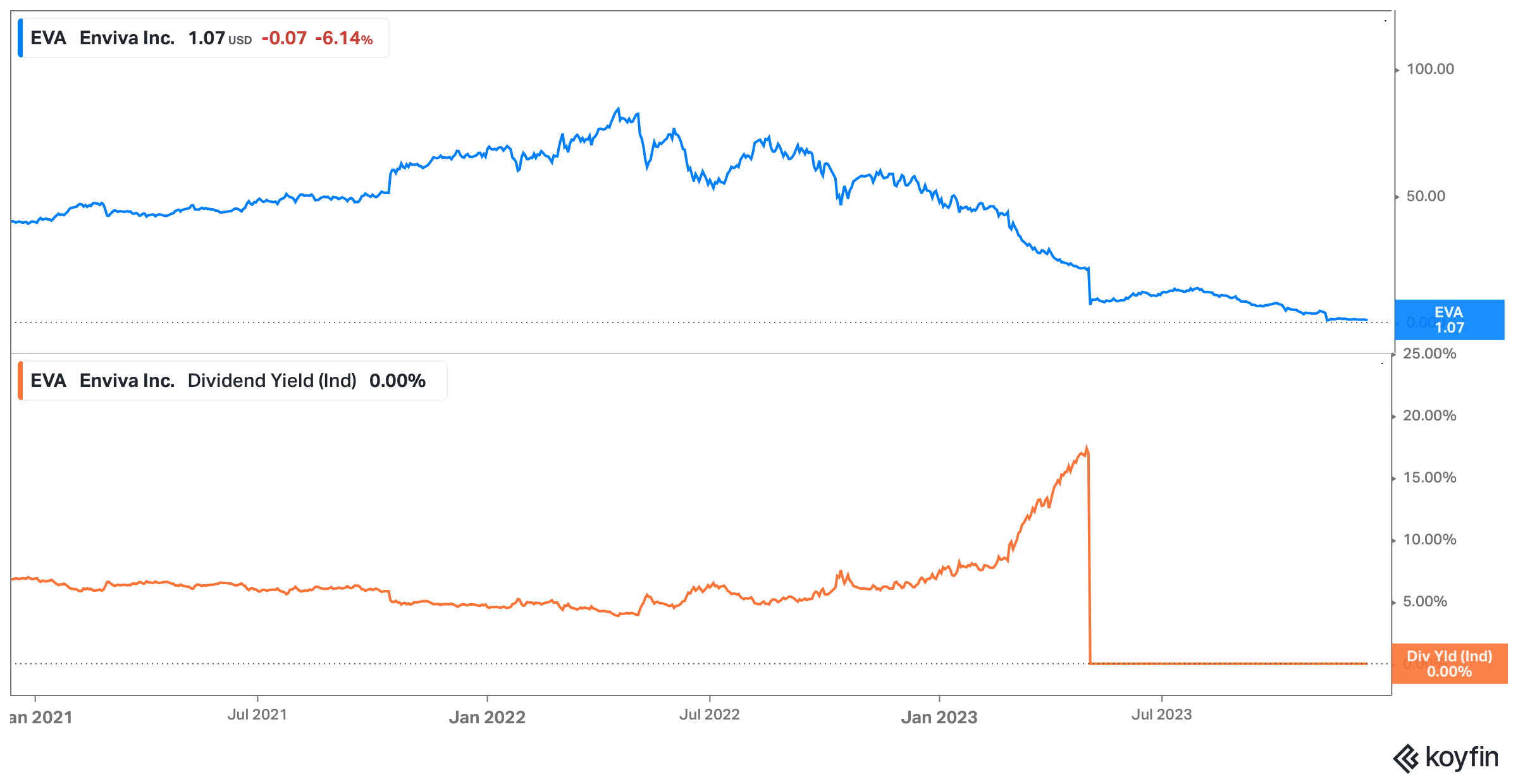

Our first piece in this series, on Walgreens Boots Alliance WBA 0.00%↑, too highlighted the danger of chasing yield. Enviva EVA 0.00%↑, which we covered in June, had just eliminated its dividend; the stock plunged 67% in a single session and has fallen another 85% since.

Source: Koyfin.

Even if the stock doesn’t necessarily collapse, there is an opportunity cost. Since the start of 2013, Hanesbrands has paid just shy of $8 in dividends, but the stock has lost $6.25 in value. Overall, even taking the dividends as cash (rather than reinvesting them as HBI fell from 2015 highs), investors over the nearly eleven years would have made about 16% total. Those who chose a simple index fund, the S&P 500 Total Return SPY 0.00%↑, generated returns of nearly 300%. Even in a zero-interest-rate environment, a traditional savings account or CD (certificate of deposit) would have done better.

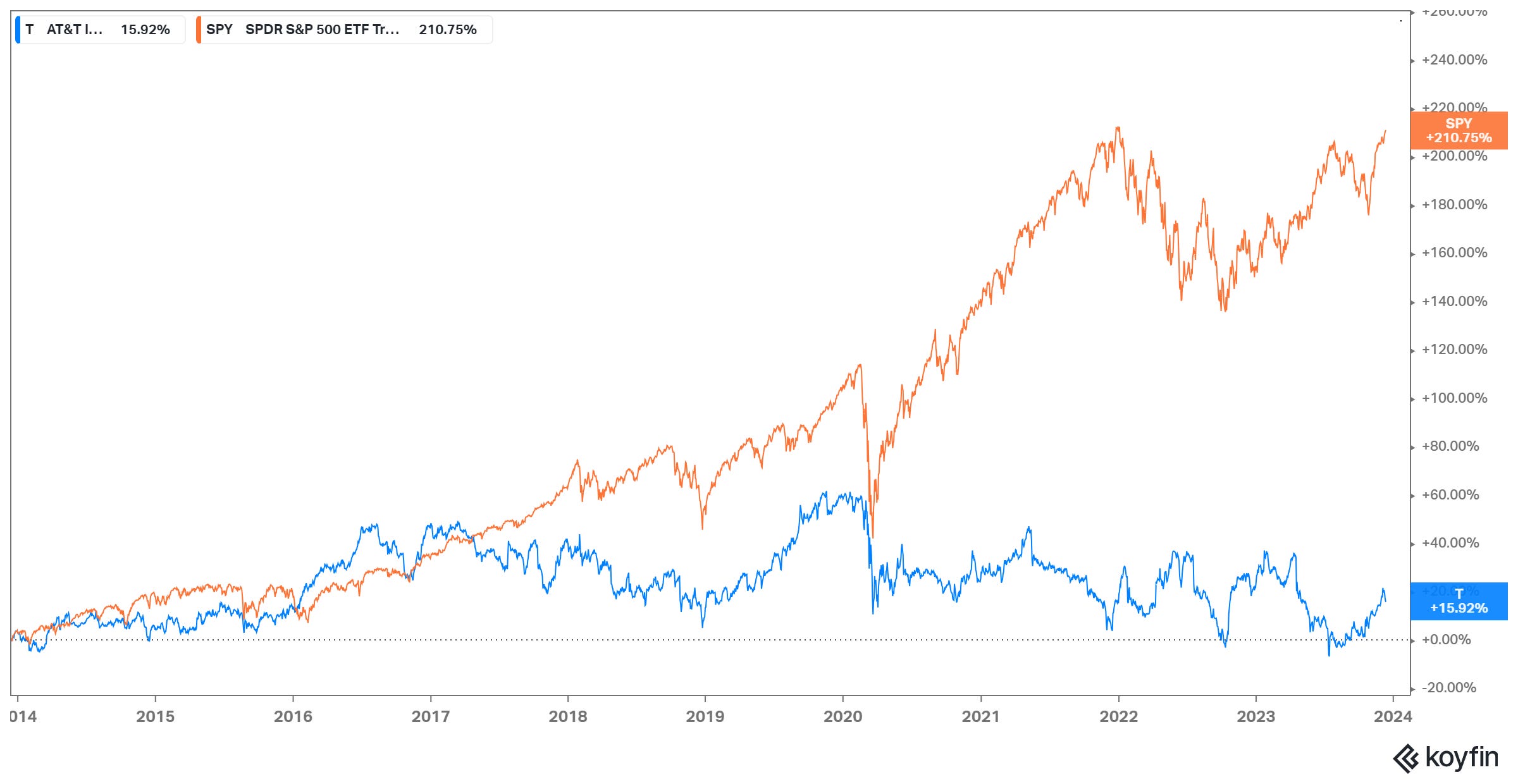

AT&T stock is another classic example. That stock is one of the most popular among income investors because not only has it almost always offered a high yield, but it ‘seems’ safe. Wireless providers don’t have a ton of macroeconomic exposure (it takes financial disaster to cancel one’s wireless plan) and the AT&T brand is one of the most well-known in America.

As a result, investors have been chasing yield in T for years and have been punished with startling underperformance:

source: Koyfin; 10-year chart of total returns in T and SPY

Yield Is Not Additive

But perhaps the most basic misunderstanding of dividend yield is that a dividend is not additive in the way that an interest payment is. An interest payment is added to the principal. A dividend payment, however, comes out of the earnings of the business, and thus comes out of the value of the business. If a company distributes cash worth 1% of its market capitalization, all else equal the next day the market capitalization should be 1% lower.

And so investors don’t come out ahead. Essentially, 1% of their investment was transferred from ownership in the business to cash. That’s a hugely important point to make: a dividend payment is simply the transfer of control of a small part of a company’s cash to its shareholders. One day, the dividend payment is in the corporate bank account. The next3, it is in the bank account of the company’s shareholders.

Special dividends provide a clearer way to highlight the mechanics. Imagine a stock that trades for $15, and the company has $5 per share in cash. The company then declares a $4 per share special dividend.

The valuation of the company plus that cash hasn’t changed4. And so after the special dividend payout, the stock should drop to about $11 (though other factors may affect trading somewhat). On the ex-dividend date5, shareholders owned a business, roughly speaking, worth $10 per share and with corporate cash of $5 per share. On Thursday, shareholders own a business worth $10 per share, corporate cash of $1 per share, and have an additional $4 per share in cash in their accounts. The math essentially gets to $15 per share on both days.

Why Dividends Are Overrated

Essentially what this means is that all the coverage given to dividend stocks, all the paid services, and the fact that dividend yields are considered one of the most important financial metrics are, in a sense, much ado about nothing.

But, again it’s more nuanced because it’s important to understand why some companies pay dividends and others don’t. While individual cases vary, the broad distinction is that dividend payers don’t have an appropriate use for all of the capital they are generating. Those companies can reinvest current earnings into management’s eighth-best idea to increase future profits, or give a portion of those earnings to shareholders who can invest it in their best idea (which sometimes is simply more shares of the company’s stock).

Basically, companies start paying dividends when they don’t have any better ideas6. But companies with significant growth ahead do have better ideas, and potentially high-return opportunities to allocate current earnings (acquisitions, increased short-term spending to drive long-term revenue, new businesses, etc.).

This in turn colors the idea that dividend stocks intrinsically are better, an argument some investors make. Those investors would argue that while dividend cuts do occur, that doesn’t mean dividends should be ignored altogether. They’d also point out that dividend stocks historically have outperformed the market.

But the outperformance of dividend stocks at least in part is based on confusing correlation for causation. Dividend stocks outperform not necessarily because it’s better to pay a dividend, but because the kinds of stocks that pay dividends likely offer a better profile. They are more mature, usually profitable, and often more defensive (in other words, less susceptible to macro cycles that can wipe out an investment).

There’s also huge survivorship bias at play: companies that maintain their dividends almost by definition are good companies, and thus substantially more likely to be good investments.

To be clear, this is not to say that dividends are bad, or that dividend stocks should be avoided. Rather, it’s to highlight a hugely important point: dividend stocks are just stocks. The fact that they pay a dividend in nearly all cases actually has a nearly-immaterial impact on any detailed calculation of fair value.

Watch Out For High Yield

In fact, high yield usually is a signal of danger, not opportunity. Over the long-term, high-yield stocks have shown some evidence of outperformance: the highest-yielding members of the Dow Jones Industrial Average, for instance, did better over a quarter century from 1987 to 2012.

But an investor should understand why a stock — or any investment — has a high yield. The working presumption should always be that the market is pricing in higher risk. It expects profits to decline and/or the dividend to be cut. In the bond market, where interest rates are almost always fixed against the par value of the bond, yield rises as price declines. Outside of dramatic changes in interest rates (like that seen over the last 21 months), that higher yield almost always means higher risk.

At the very least, a stock cannot be bought just for its yield. The reasoning there is simple, and part of a theme we’ve emphasized throughout this series: successful investing is hard. The idea that one single, widely available metric means a stock is a buy ignores that immutable fact. But the nature of yield elsewhere in finance makes it easy to fall into that trap. As we noted in May, even professionals make simple errors when it comes to dividends and buybacks.

Admittedly, it might seem contradictory to argue that a high dividend yield is nearly meaningless as a reason to buy a stock, but worth noting as a reason not to buy a stock. But the reason a high yield can be a red flag is not intrinsic to the size of the dividend payment, but rather due to the correlation between a dividend and earnings.

Dividends come out of profits, and when a yield goes up it’s almost always because the earnings multiple (and usually the stock price) is going down. And when the earnings multiple is going down, that in turn is a sign that the market is pricing in lower expectations for future profit growth. And it’s that profit growth that really matters, not a single metric that discloses how much of that profit shareholders are getting at the moment.

If you enjoyed this article you can helps us by sharing it or clicking the ❤ button.

As of this writing, Vince Martin has no positions in any securities mentioned.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

In the olden days, banks did fail, and depositors lost some or all of their principal as a result. But in the U.S. at least, the current regulatory regime effectively guarantees deposits. It’s hard to imagine even a hypothetical situation in which a U.S. customer can’t get her deposit back.

Outside the U.S., dividend policies are quite different. Often, corporations pay a predetermined amount after the first half of the year and then a variable dividend at year-end depending on performance. There are exceptions in the U.S. as well. Realty Income O 0.00%↑ famously pays dividends on a monthly basis; it’s even trademarked the phrase “The Monthly Dividend Company”. A few companies issue variable dividends, and so-called “special dividends” are telegraphed as being one-time, as opposed to consistent payouts (referred to as “regular dividends”).

We’re oversimplifying here. Technically, payments take more than one day, and there are tax considerations as well which mean, in a few cases, not all of the cash does go directly to shareholders. But the broad point holds.

Here, too, we’re oversimplifying somewhat. The transfer of cash from the corporation to shareholders could be seen as a positive, if investors were previously worried management might spend that cash imprudently. But that good news, as it were, presumably would be priced in after the announcement of the special dividend, not the payout, which usually comes a couple weeks later.

The last day to own the stock and still receive the dividend; you can read about the mechanics here.

They can also do so when they simply generate more cash than they know what to do. Apple AAPL 0.00%↑ and Meta Platforms META 0.00%↑ are in this situation, though both companies are returning capital to shareholders in the form of stock buybacks rather than dividends.