Research Notes: AI Stocks Are Not What They Seem

The current AI frenzy is creating short opportunities — but also vexing long-term questions

We’ve clearly entered a hype cycle for artificial intelligence. The launch of ChatGPT in November brought AI into the mainstream, and since then stocks with perceived exposure to the trend have soared. More broadly, we’ve seen increasingly aggressive projections of what generative AI, in particular, might look like.

Here’s Microsoft co-founder Bill Gates on his personal blog last month:

The development of AI is as fundamental as the creation of the microprocessor, the personal computer, the Internet, and the mobile phone. It will change the way people work, learn, travel, get health care, and communicate with each other. Entire industries will reorient around it. Businesses will distinguish themselves by how well they use it.

There’s some reason for skepticism toward the stocks and also the perception of the broader trend. It’s not that AI isn’t transformative. It’s that avenues to profit are exceedingly narrow.

A decade ago, 3-D printing was supposed to “change the very nature of manufacturing, alter the global trade balance, and potentially spark a new industrial revolution.” 3-D printing stocks soared and eventually, and inevitably, crashed back to Earth.

That trading (and market history more broadly) suggests that the current AI hype cycle is going to lead public market investors to lose a lot of capital, and create short opportunities for traders that get the timing right. But there is a case that this time might be slightly different.

The AI Hype Cycle

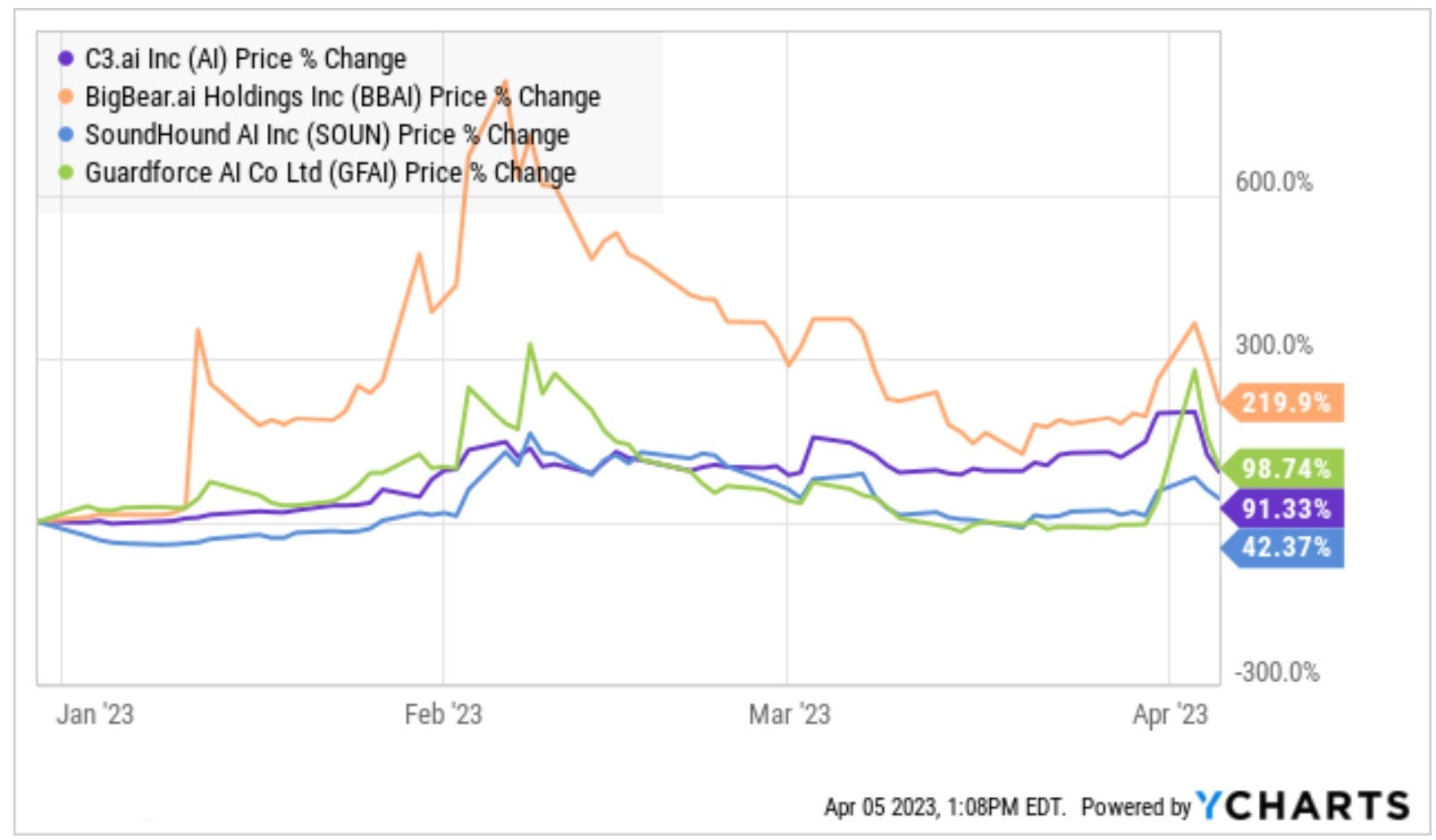

Let’s be clear: there’s clearly a hype cycle in AI. A basket of four stocks with “AI” in the name is +113% year-to-date:

source: YCharts

There have been secondary winners as well. Nvidia NVDA 0.00%↑ has surely benefited. What other explanation is there for the ~$300 billion in added equity value so far in 2023?

Companies are doing their part as well. For the first quarter of 2023, there are easily more than 200 (we stopped counting, to be honest) mentions of artificial intelligence in company earnings calls. That includes transcripts from leaders like Coca-Cola KO 0.00%↑ and Kilroy Realty KRC 0.00%↑.

The financial media is jumping into the fray as well. The Motley Fool pitched a webinar on the topic, and is offering access to an “A.I. Profit Playbook” for the low low price of just $249:

An Easy Short — Right?

For the more direct names, there seems reasonably solid short cases. Kerrisdale Capital has already come out swinging against C3.ai AI 0.00%↑. Last month, the firm called C3 "a minor, cash-burning consulting and services business masquerading as a software company". This week, the company even sent a letter to C3's auditor alleging “highly aggressive accounting”.

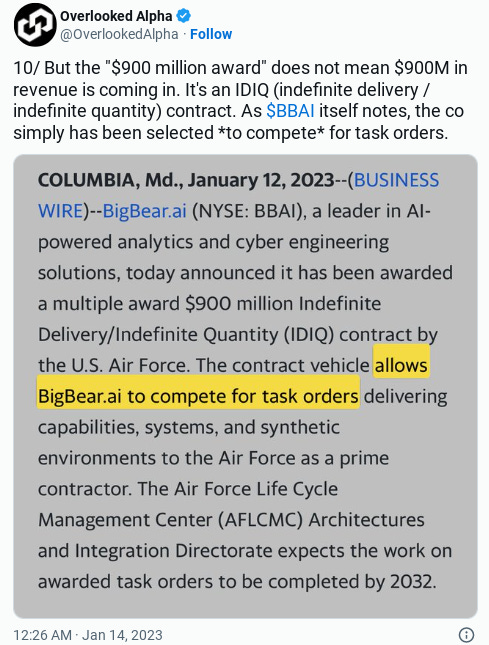

Back in January, on Twitter, we noted our skepticism toward BigBear.ai BBAI 0.00%↑whose stock more than tripled in one session after it announced a contract win with the U.S. Air Force. That contract, however, seems to have been misinterpreted by the market.

Kerrisdale’s trade has worked so far, thanks to a 38% plunge in AI stocks over the past two sessions. BBAI has followed AI down, but the short case there still looks attractive. The business isn’t even growing, Adjusted EBITDA is negative, and yet the debt load is greater than the market cap.

Conversational AI provider SoundHound AI SOUN 0.00%↑ ostensibly is trying to be the next LivePerson LPSN 0.00%↑. But LivePerson has an enterprise value of $650 million and trades at ~1.3x 2022 revenue. SoundHound is already worth ~$400 million, 13x 2022 revenue and it isn't clear why. Guardforce AI GFAI 0.00%↑ has a $10 million market cap and just executed a 1-for-40 reverse split.

More broadly, the point is that the current crop of “AI stocks” aren’t really “AI stocks”:

C3 and SoundHound are not developing the next iteration of ChatGPT any more than Canopy Growth CGC 0.00%↑ was going to be the next Anheuser Busch InBev BUD 0.00%↑ or 3D Systems was going to power a worldwide network of specialized micro-factories. Meanwhile, if you look at the company behind ChatGPT, OpenAI started as a non-profit and it's clearly nowhere close to being a public company. The idea that you can find the next 'Amazon' in the current crop of AI stocks seems far too optimistic.

We have been here before. Over and over again. Sure it’s possible the likes of Nvidia or Alphabet GOOG 0.00%↑ GOOGL 0.00%↑ could, over time, drive material revenue and profits from generative AI. But those companies are already so valuable that the definition of "material revenue" requires certainty that simply doesn't exist.

And there’s another problem here: timing. If you look back at 3-D printing stocks, there were pullbacks early in the trend that look much like this week’s plunge. Optimism, however, would resume.

The fact that 2013 was a hot market for tech (the NASDAQ Composite rose 38%1 after a 16% jump the year before) may have helped. Still, short sellers in the likes of 3D Systems DDD 0.00%↑ or Stratasys SSYS 0.00%↑ relearned the old adage that, from the short side, being early is the same as being wrong2:

source: YCharts

It’s not hard to see a similar risk here. BBAI looked like a screaming short after its 260%, one-day rally in January. Immediately fading the stock would have worked exceptionally well: shares are down 28% from that close. But to achieve those gains, a trader would have had to hold on through an ensuing rally that led the stock to double. Holding firm against those trends is often easier said then done.

The Right History

In other words, we’re at the point in the AI trend where history suggests the wisest decision, at least for public market investors, is to do nothing. At some point, short opportunities will arise, and those opportunities will be better attacked six months too late than six days too early.

But that’s only true if we’re applying the right history. If generative AI is closer to 3-D printing, or cannabis, or U.S. online sports betting, than (as Gates and others are arguing) the Internet or the smartphone.

It does seem like the optimists, in this case, might be right. It’s hard from the outside to precisely assess ChatGPT’s current capabilities. It’s alternately passing difficult exams and baldly failing basic arithmetic. Going forward, however, a flood of capital and development is going to lead to exponential improvements from whatever the current base is. Meanwhile, a “full-blown mania”, as the New York Times put it, among venture capitalists is likely to steer billions of dollars into the space.

But, being optimistic and right still requires patience, as we learned in the late 1990s. The Internet was as transformative as optimists believed, but valuations went haywire and some of the early leaders (AOL and Yahoo! being prime examples) fell by the wayside.

Still, if generative AI does meet expectations, it’s not too early to start considering winners. One very real question, however, is whether there might be any winners at all.

The Optimistic View Of Generative AI

It doesn’t take a Luddite to have some skepticism, and even fear, of generative AI. Last week, a group of experts publicly called for a six-month pause in development of AI systems until “we are confident that their effects will be positive and their risks will be manageable.”

But even excluding the development of an artificial general intelligence that decides to enslave all mankind, there is a clear potential downside too. Generative AI has the potential to replace existing jobs3 , and if it replaces too many jobs the net impact on the global economy could be sharply negative.

I mean…assuming continued development in generative AI over the next decade, do financial writers even exist anymore? Do individual investors even exist anymore?

Those questions are particularly important from a selfish perspective, but they get to broader concerns. The financial sector accounts for more than 7% of U.S. gross domestic product and is a key component of modern economies.

In that space, however, we do have precedents:

The development of the spreadsheet, over time, wiped out the bookkeeper. But that same development created many more white-collar jobs for those who could analyze and act on the better (and better-presented) data available under the new paradigm.

And so the optimistic view here is that generative AI, like the spreadsheet, will destroy current jobs but create new ones. That in turn should boost economic growth. ARK’s Cathie Wood last year argued the growth rate could get to 30%-50% annually, and while that was my personal nomination for the dumbest tweet in history, more sober and reasonable observers can share her optimism in kind if not in degree.

Again, patience is required. It took years for the Internet to truly create significant, market-beating returns (one could argue it took ~15 years, in fact). There was a surprising number of ways to lose money on the stunningly fast smartphone trend as well.

But there is a way to view the launch of ChatGPT as the beginning of a multi-year tailwind for worldwide economic growth and equity values, even if the distribution of that growth and that value will be sharply uneven.

Two Reasons For Pessimism

Yet there’s a pretty strong case for taking a bearish view toward AI longer-term. We see two core reasons for doing so.

The first is that generative AI needs to be good — but not too good. The blue-sky scenario for the technology seems almost certainly to imply a level of disruption that us mortals are simply not prepared to handle well. The worst-case scenario, in other words, is not that generative AI proves to be a disappointment, but that it proves to be an irresistible and unstoppable success.

It’s tempting to argue that this outcome, should it even occur, is decades in the future. But one does wonder if early success in generative AI could have near-term implications in terms of valuations, as investors apply larger and larger haircuts to terminal value in so many sectors.

Substack itself, for instance, is selling equity to its writers. But revisit our question before. Does human-generated financial analysis or political commentary or scientific coverage exist in a decade? That is a real question when considering an investment in Substack. And over time, it will become a real question in many other sectors as well. An AI-driven world in theory should be a much faster-changing world, if only because there are fewer dumb humans to act as friction. A faster-changing world is one in which the present value of future earnings is sharply reduced.

The irony here is that an uber-bull on generative AI probably shouldn’t be looking for AI plays. She should probably be preparing for an exponentially larger version of “The Big Short” — The housing trade from the late 2000s. A world truly disrupted by generative AI is a world in which many industries collapse, governments fall and companies go from leadership to bankruptcy in a matter of years. It is a world flooded with potential short opportunities.

The second case is that there’s actually a far more pessimistic precedent for AI beyond the spreadsheet-driven demise of the bookkeeper. In the 1960s, the rise of robotics was seen as a threat by American labor unions, to the point that they repeatedly fought their installation in U.S. factories. We can look at that history, six more decades of GDP growth in the U.S. and worldwide, and presume that the arrival of robotics had a massive net benefit.

That may be true — but a key word there is “net”. A good swath of the U.S. is still referred to as the “Rust Belt”. Cities like Gary, Indiana and Youngstown, Ohio never recovered. If AI’s reach exceeds that of manufacturing robots (as seems likely) how big does the “Rust Belt” become?

Again, it’s far too early to have any certainty on what generative AI looks like. But it does seem like this already is a different world, with more change on the way. It does seem like this isn’t just 3-D printing all over again. And, for investors, it does seem like generative AI is going to create opportunities to make — and to lose — an awful lot of money.

As of this writing, Vince Martin has no positions in any securities mentioned.

If you enjoyed this post you can help us by clicking the heart ❤️

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

Not going to lie: I did not remember that at all.

Investors familiar with Proto Labs PRLB 0.00%↑ might object to the company being in this group, as it wasn't and isn't a 'true' 3-D printing play. But that goes to the point of the mania: it was clearly treated as such at the time, whether that was true or not.

One interesting investing question beyond the scope of this article at the moment: what company has the greatest percentage of its cost base tied up in those kinds of jobs, and thus the greatest mid-term potential for savings?

"C3 and SoundHound are not developing the next iteration of ChatGPT any more than Canopy Growth CGC 0.00 was going to be the next Anheuser Busch InBev BUD -0.09%↓ or 3D Systems was going to power a worldwide network of specialized micro-factories."

Got a good chuckle. Good piece

As almost always seems to be the case, I agree with most of your investment conclusions.

Investing aside, if there is a systematic error in evaluating generative AI, it seems more likely that the error is in underestimating its technological potential and societal impact based on its current capabilities.

Consider, for example, that GPT-4 is "10 times more advanced than its predecessor, GPT 3.5".

https://www.searchenginejournal.com/gpt-4-vs-gpt-3-5/482463/#:~:text=GPT%2D4%20is%2010%20times%20more%20advanced%20than%20its%20predecessor,more%20accurate%20and%20coherent%20responses.

I don't know if 10x is the right number, but for the purposes of this thought experiment it doesn't much matter. Consider how long it took to go from v 3.5 to v 4.0, and now compound that rate of progress. Over 12 months. 24 months. Ten years.

With apologies to Albert Einstein (I'm no Albert Einstein) and his Eighth Wonder of the World, the implications of what we've stumbled upon are truly mind-boggling.