Highlights:

A strong quarter from Viator highlights the bull case for TripAdvisor — but the case isn’t airtight.

“Return on brain damage” ends the TSLA short.

EWCZ is down 14% since we laid out the bear case; an ugly Q3 suggests more downside ahead.

TripAdvisor: The Viator Catalyst

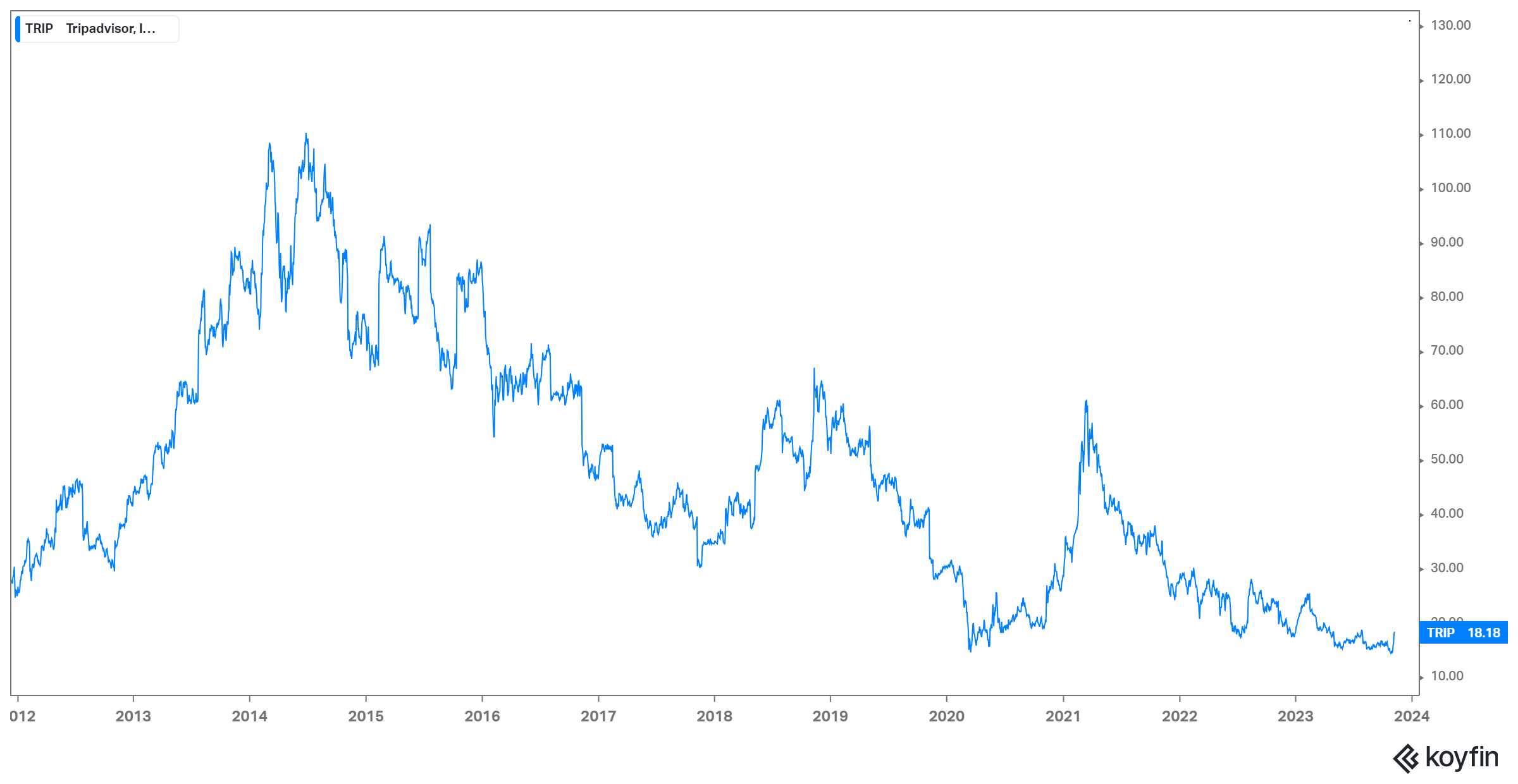

TripAdvisor TRIP 0.00%↑ is down about one-third since its spin-off from IAC nearly twelve years ago. But that long-term decline has included some very steep rallies:

source: Koyfin

Starting in late October 2012, TRIP gained more than 250% in less than 17 months. From November 2017 to November 2018, shares better than doubled. The stock quadrupled off COVID lows in less than a year.

In other words, if an investor catches TRIP right, she can catch it very right. And there’s one reason to see history repeating here: Viator, TripAdvisor’s experience platform. Viator is growing nicely, and that doesn’t seem priced in. Based on guidance given after this week’s Q3 earnings release, TRIP is trading at less than 8x this year’s Adjusted EBITDA.

There’s reason to think that Viator should drive that multiple much higher. In 2019, the business generated $288 million in revenue, while posting an Adjusted EBITDA loss of $28 million1. Last year, revenue was $493 million, albeit with a small loss; post-Q4 guidance suggests this year’s print should be about $730 million, with EBITDA running around breakeven.

That’s a four-year annualized growth rate of about 26%. And if you squint, there’s an argument that Viator supports something close to the entirety of TripAdvisor’s $2.24 billion enterprise value.

Can Viator Make TRIP A Multi-Bagger?

That sounds insane at first, but it’s perhaps not that crazy. A 3x revenue multiple is in the range of Booking Holdings BKNG 0.00%↑, Uber UBER 0.00%↑, and Etsy ETSY 0.00%↑. Viator almost certainly isn’t as good a business as those giants, but it is (for now) growing faster. A take rate which has remained over 20% of gross bookings suggests some real pricing power relative to suppliers, and further supports the idea that this is perhaps a better business than investors in the public market might realize.

Investors in the private market certainly like the industry. In June, Viator rival GetYourGuide raised $194 million at a valuation just shy of $2 billion, which included fresh funds from giants KKR KKR 0.00%↑ and Singapore’s Temasek. GetYourGuide (which is headquartered in Berlin, and for now has more of a European focus) hasn’t disclosed revenue, but TripAdvisor has repeatedly called Viator the largest player in the space.

Even assuming that the headline valuation for GetYourGuide’s raise is inflated (as most are, for public relations purposes), assigning that peer multiple to Viator probably accounts for the entirety of enterprise value (or very close). That in turn leaves a core business still generating $300 million-plus in annual EBITDA available essentially for free (or, again, very close to it).

And with TRIP gaining 11% Tuesday off Q3 earnings, there’s a case that a broad sell-off in travel stocks — the ETFMG Travel Tech ETF AWAY 0.00%↑ dropped 20% between July 31 and Oct. 27 — led investors to discount the Viator story too much.

What Goes Wrong For TRIP

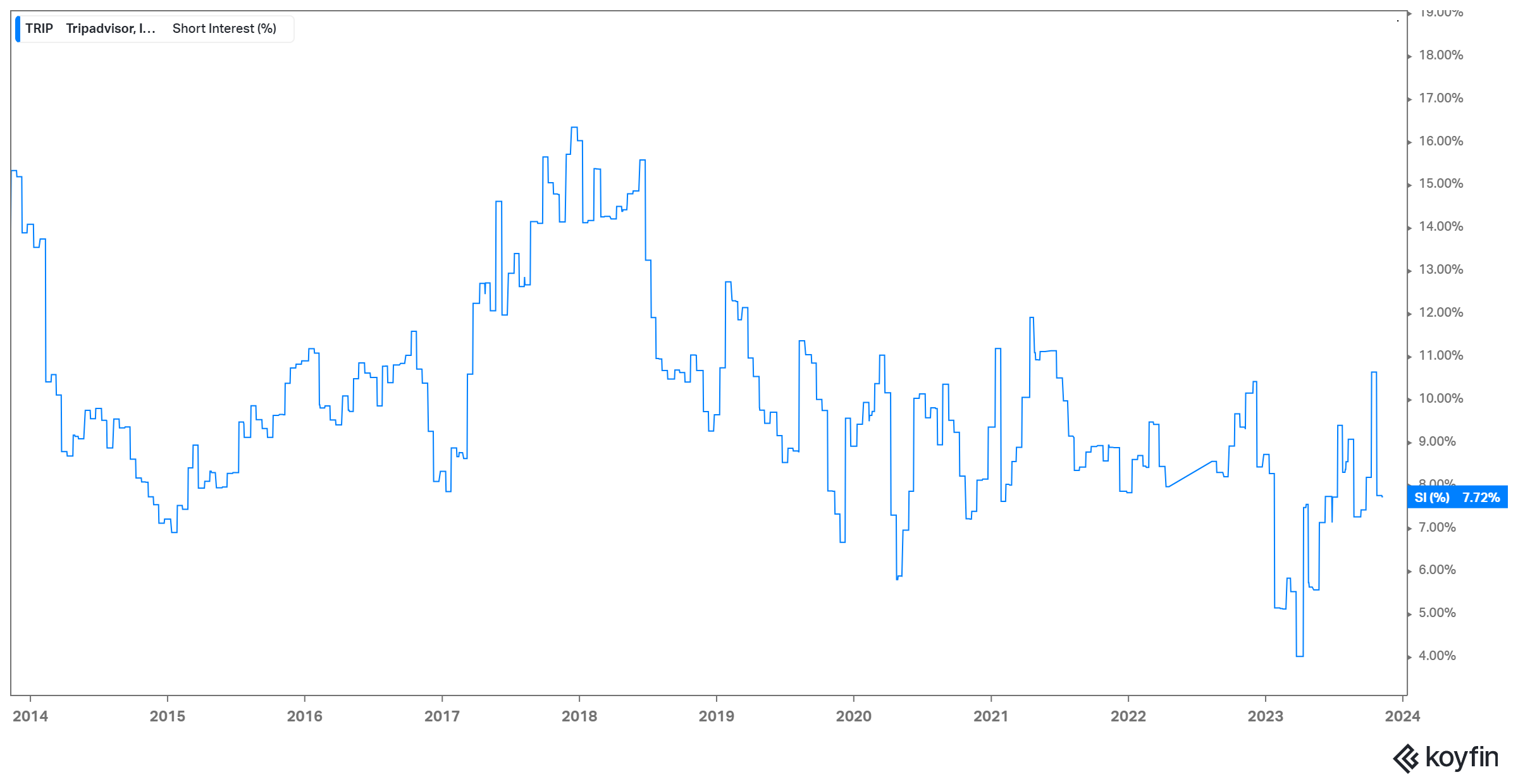

It’s an intriguing story, certainly. But many investors don’t believe it. Over 10% of the float remains sold short, as TRIP continues to be a reasonably popular bear target:

source: Koyfin

Broader caution toward travel certainly seems wise at this point after two years of pent-up demand. It would seem possible, and maybe likely, that Viator would have received an exaggerated benefit from that demand, with travelers spending more and going on more exotic, experience-driven trips after the pandemic.

There are structural concerns as well, highlighted by the fact that Viator still isn’t profitable. Incremental margins have been basically zero: in the first nine months of 2019, Viator generated a $24 million Adjusted EBITDA loss, and with revenue $350 million higher this year the loss has narrowed by just $9 million. The obvious question is whether there’s really an overarching ‘brand’ to be had in experiences, or if Viator’s revenue growth is being acquired by spending heavily on marketing into a still ‘hot’ market. If it’s the latter, then the business simply isn’t that valuable, and the valuation assigned to GetYourGuide is just a misstep by aggressive venture capitalists.

There is also the fact that the core business seems to be in very real trouble. In 2019, the Core segment generated revenue of $1.22 billion and Adjusted EBITDA of $476 million. The figures this year should be about $1 billion and $340 million, respectively. On the Q4 2022 conference call, TripAdvisor management all but admitted that the business was never going to return to 2019 levels, in large part because of weakness in categories like cruises and rental cars.

In that context, the bull case here gets difficult. If Viator isn’t quite worth $2 billion, and Core is really a 4x-6x EBITDA business, on paper there’s still a case for 50% upside2. But as we’ve discussed before, upside “on paper” is the biggest risk to these kinds of bull cases. Even the current price rests on pricing Viator as a legitimate, permanent, platform business. It might be a little early to make that bet; TRIP looks like one of those plays where it might be better to own at a higher price with more information, rather than taking the gamble on a long-term underperformer whose value proposition hasn’t yet been proven.

Tesla Stays Flat

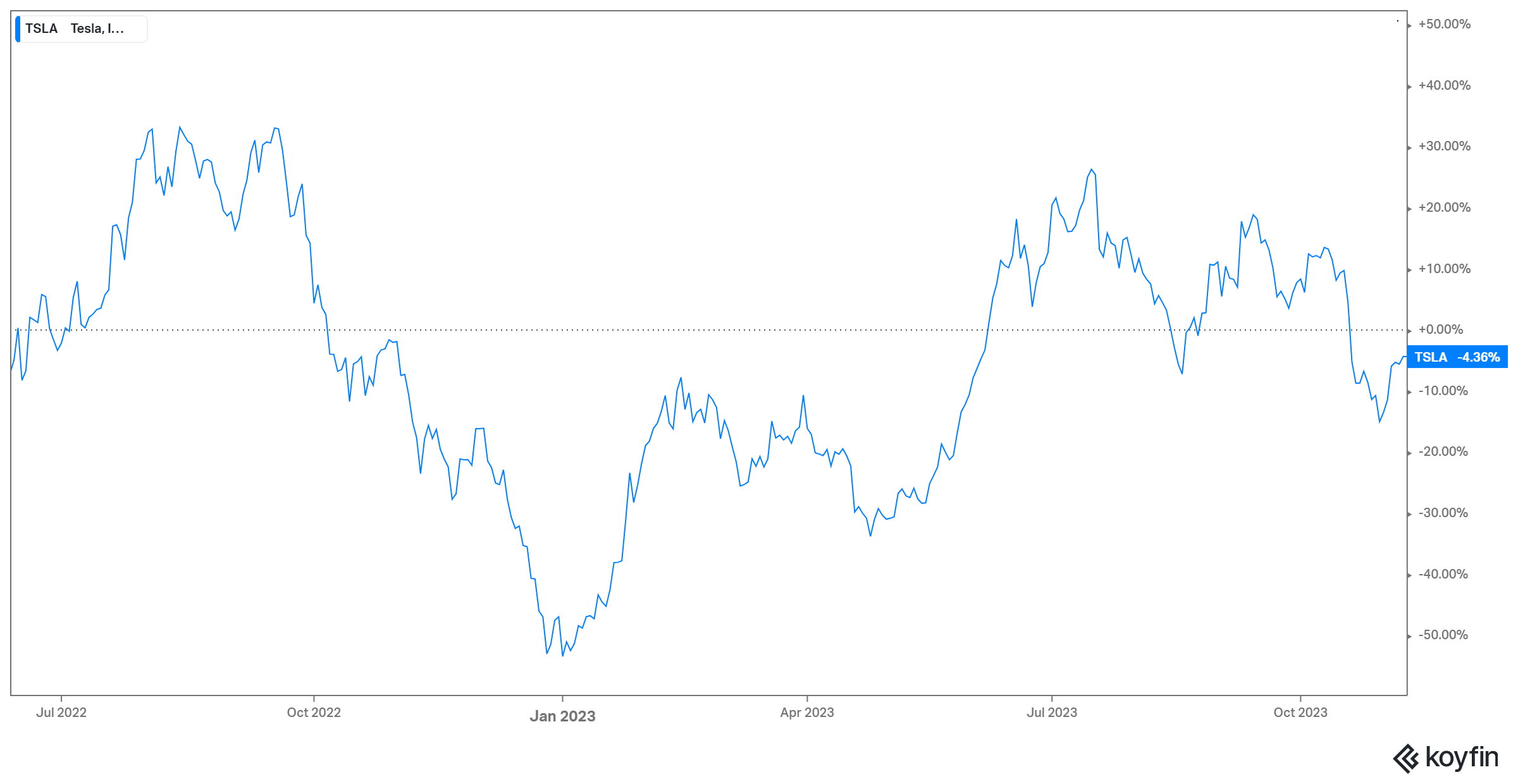

16 months ago, we laid out the short case for Tesla TSLA 0.00%↑. We argued that looking at TSLA as “just another stock” suggested material downside.

The case wound up playing out quite well through the end of 2022, at which point I should have covered. I didn’t and a strong rally this year leaves the stock almost exactly flat to our recommendation:

source: Koyfin; chart since 6/12/22