Research Notes: Risky Stocks Rally

Thoughts on Nikola, Plug Power, Trupanion and Affirm.

Highlights:

Speculative stocks are roaring again. But the last time that happened, it signaled a top.

We update the Sh—tco rule of 100 and consider an options trade in Nikola.

Plug Power has too many questions and not enough answers.

Affirm is a popular short, and for good reason.

The recent market rally faces no shortage of skeptics. The S&P 500 Total Return has gained 15% this year based largely on contribution from a relatively small number of constituents. Just 23% of the index’s stocks outperformed in May, the smallest such percentage since 1986. One of the stocks driving those gains is Nvidia, which some investors view as being a beneficiary of a bubble in artificial intelligence1.

Macro pressures remain. Inflation is moderating but still high. The U.S. consumer, surely, can’t keep spending like this forever.

On top of it all, it seems like a lot of weaker names have performed exceptionally well of late. Among small-cap ($300 million) or larger stocks, two of the four best performers in 2023 are crypto miners Bit Digital and Cipher Mining. Three more miners are in the top 20.

Carvana is 5th. BigBear.ai and C3.ai are 13th and 15th, respectively. The reasons don’t seem to go far beyond the “ai” in their corporate names. Fellow AI(ish) play Symbotic has added ~$18 billion in market capitalization in less than six months.

Speculative stocks — many of which were left for dead in 2022 — have roared back in 2023, particularly over the last few months. Given that many of those names declined in 2022 for appropriate reasons, skepticism seems well-founded. When these kinds of stocks go crazy, it’s often a sign that a reversal is on the way. Indeed, that was the case less than a year ago.

The Sh—co Rule Of 100

Last year, we launched the Sh—co Rule of 100 Index, a quick-and-dirty list of the market’s weakest stocks. Here’s the current list:

[Score equals current short interest as % of float plus inverse of 1-year performance. Minimum market cap $300 million; minimum short interest 15%. Score as of the close on Wednesday 6/21. Data from finviz.com.]

Novavax - 120

Nikola - 109

Allogene Therapeutics - 104

ZIM Integrated Shipping Services - 104

Fate Therapeutics - 103

Enviva - 100

PacWest Bancorp - 96

Blink Charging - 95

Beyond Meat - 93

Trupanion - 91

This ‘index’ is far from exhaustive, and mostly tongue-in-cheek. Still, it provides a good sample of the most popular “short to zero” bear cases in an environment where it still feels a little dicey to short anything to zero.

And over the past month, these ten names on average have rallied more than 16%, roughly triple the gains in the Russell 2000 Total Return.

We’ve been here before. Back in mid-August, we updated our original list,2. The top eight names on the list in early June had, in eleven weeks, gained an average of 45%. Carvana led the way with an 82% gain, regaining the $50 level in the process.

That update took place right here on the Russell 2000 chart:

source: finviz.com (author highlighting)

Over the rest of 2022, those same eight stocks declined by an average of 62%.

Weak names can rally for all sorts of reasons: short covering, “long volatility” strategies, retail interest, yield-chasing. But almost by definition, the rallies are unlikely to last.

We’re probably not quite at the point we were in mid-August, when we top-ticked the group pretty much to the day3. But there are some signs that if the entire market is not necessarily a short (and on that front we’re not yet convinced), its more speculative names are getting in range. And so we’ll take a look at a few of those intriguing short cases here.

The Original Plan for Nikola

Following the scandal involving Trevor Milton, the founder of Nikola who was later convicted of securities fraud for false claims about the company, a key part of the Nikola story was was obscured. Milton’s claims, along with the infamous video of Nikola pretending a “pusher” was self-propelled (it actually was rolling down a gentle slope), gave many investors the impression that Nikola’s strategy rested on technical superiority and/or innovation.

To some degree that was indeed true. But Nikola’s business model was as much financial as technical. I made this point elsewhere a couple of years ago, but when Nikola announced its merger with a SPAC (special purpose acquisition company) in March 2020, its management was clear about where its edge lay. It wasn’t in technical expertise; the host of “partnerships” involved in building the projected vehicles (both battery- and fuel cell-powered) proved as much.

Rather, particularly in fuel cells, Nikola posited that its advantage would be the ability to offer defined total cost of ownership on a multi-year basis to trucking customers. This is why the company planned to spend nearly $20 billion building out a nationwide network of fueling stations. That network, plus in-house maintenance, meant that Nikola could offer what it called “bundled pricing” on a 7-year/700,000 mile basis.

Once Milton was removed and NKLA stock imploded, that model created two key problems. The first was that the lower NKLA stock price itself harmed the company’s prospects, since at a certain point it could no longer raise the capital needed to fund such grand ambitions via equity sales. The second was that when the model tanked, there was nothing really left. A business model based on technical engineering might have some value to salvage. One based more on financial engineering had no floor.

Nikola’s plan has shrunk significantly. The company exited Europe, and swapped out its plan to build its own hydrogen fueling network for a series of partnerships. But the capital problem still remains. Nikola closed the first quarter with just $121 million in unrestricted cash. It burned $232 million in the quarter, and nearly $750 million in full-year 2022. Unsurprisingly, recent SEC filings contain a so-called “going concern” warning.

The one way for Nikola to raise cash is to sell equity. A $1 billion market capitalization makes this plan difficult; Nikola said after Q1 it planned to achieve positive Adjusted EBITDA by 2025. Even with layoffs, a few sales of battery-powered trucks out of inventory (which totaled $123 million at the end of Q1), and planned fuel cell-model production starting at year-end, Nikola probably needs at least $500 million to get through the next eight quarters. And it’s exceptionally difficult to raise 50% (or more) of a market cap without tanking the stock in the process.

The Proposal 2 Problem

What makes the latest rally (NKLA has gained 144% in nine trading sessions) particularly strange is that the capital raise might not be difficult, but impossible. The rally began the day before Nikola’s annual meeting on June 7. Proposal 2 at the meeting asked for shareholders to increase the number of authorized shares. The current total is 800 million; NKLA has already issued just shy of 700 million, and there are another 64 million reserved under option plans and other instruments.

Among those who voted, a majority did vote ‘yes’ for Proposal 2. But the proposal requires a majority of all shares to vote ‘yes’, and so Nikola adjourned the meeting to July 6. Still, getting those votes may prove difficult. Milton broke a multi-year silence to come out against the proposal on Instagram; he still owns ~7% of the company4. Meanwhile, Nikola itself obliquely noted that it has “a diverse stockholder base with many investors that hold small positions”. Those shareholders quite often don’t vote. This is a version of the problem that dogged AMC Entertainment, and led to the creation of its preferred stock APE.

Delaware legislators may change the corporate law currently requiring a majority of shares, instead of a majority of votes. That in turn could allow Nikola to get Proposal 2 passed later this year even if it fails on July 6. But there’s still a narrow path to survive to that point (and from there’s it’s another narrow path to surviving a few more quarters) — and huge downside if Proposal 2 fails. Nikola quite clearly doesn’t make it until the end of the year.

It’s still incredibly dangerous to short these kinds of stocks. NKLA has a triple-digit borrow rate at the moment, which doesn’t help. But the options market might provide an interesting trade. The January 2024 1/1.50 call spread, for instance, can probably be sold for $0.15 (with tons of liquidity), offering potentially 40%-plus returns if the stock dips back below $1. (If it does so consistently, a reverse split again becomes likely, and those themselves usually are negative catalysts, particularly for retail-heavy stocks.)

In the current market, a bearish trade on a highly speculative name is still an aggressive trade, obviously. But in the context of the broader story it looks like an attractive trade as well.

Believing Plug Power

I admit I enjoyed this:

source: Seeking Alpha

Analyst Day was a classic “sell the news” event. At the open on the 14th, Plug Power stock had gained 41% in nine-plus trading sessions. It’s declined 15% since. It’s not a surprise. To be blunt, this simply isn’t a company that should be believed.

Plug Power was founded 26 years ago. It spent the entirety of the 2010s promising positive EBITDA. (Current chief executive officer Andy Marsh was in charge the entire time; he assumed his post in 2008.) It hit that bogey (barely) in 2019, then guided for ~$200 million in Adjusted EBITDA in 2024. That target seems unlikely to be hit: current gross profit guidance for 2023 is just ~$140 million, with the company itself admitting to the possibility of a decline.

Shares have still bounced 33% since May, when the stock touched its lowest level in almost three years. And that alone looks a bit dicey for the market: PLUG is the kind of idea you reach for when you’re out of ideas.

Shorting the stock here admittedly is difficult (though 22%-plus of the float is sold short). This is an exceptionally complex story, requiring technical expertise about the capabilities of hydrogen (‘green’ or otherwise), an understanding of regulatory prerogatives and incentives worldwide, and predictions of the preference of corporate customers for various environmentally-friendly alternatives to hydrogen power.

The blue sky scenario here still implies a ton of upside: Plug Power is guiding for more than $7 billion in gross profit in 2030, and $4 billion in operating income. A current market cap of $6 billion probably is a 10x in that model. Still, that doesn’t mean investors should start believing management just yet.

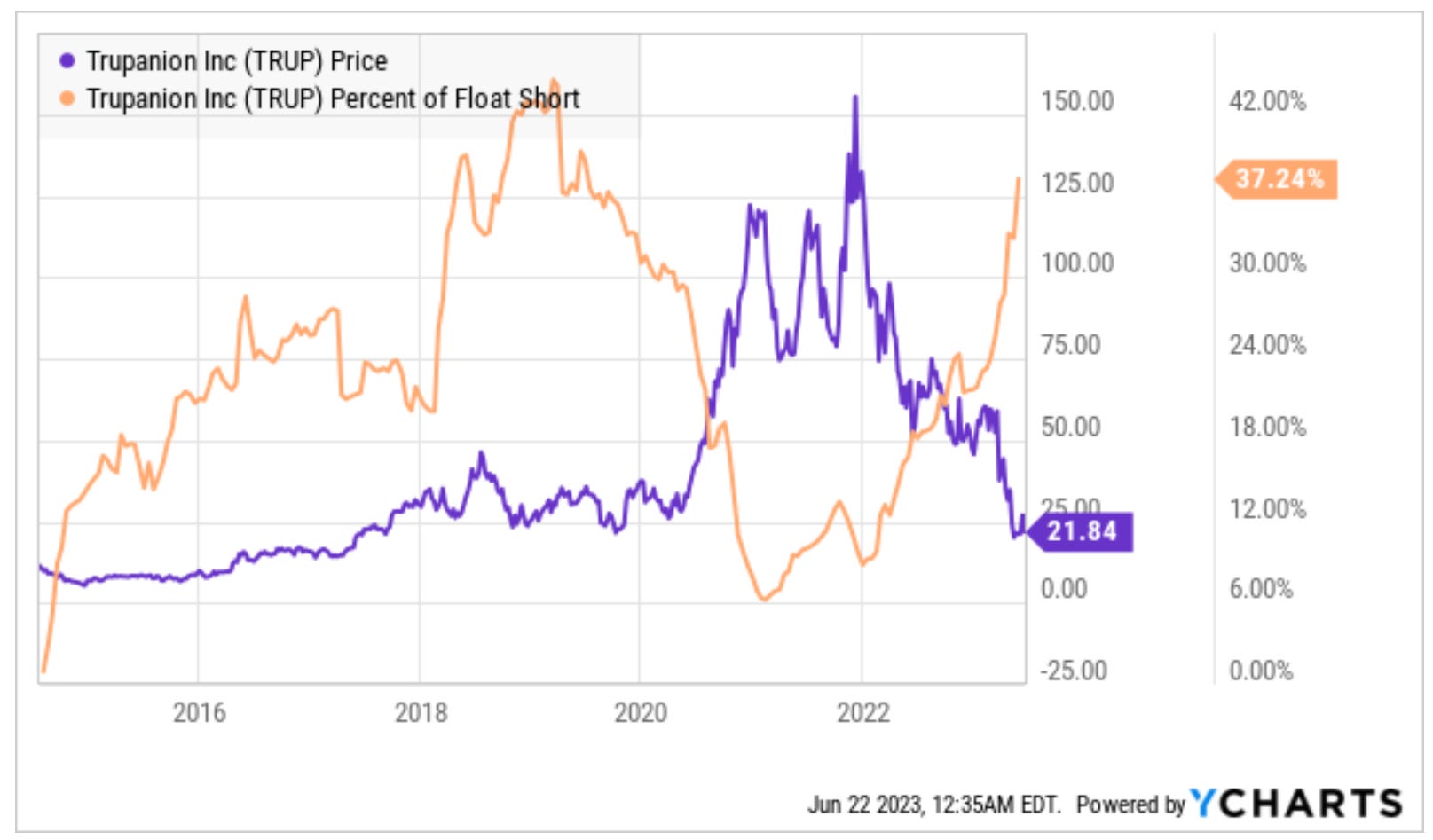

Another Shot At Trupanion

Roughly speaking, investors now can put on the same short trade in Trupanion that was popular at the beginning of 2020:

source: YCharts

That does seem attractive — though it would have been much more attractive a week and a half ago. Since then, TRUP has dropped 21%, including a 18% plunge on Wednesday.

Still, the case for shorting TRUP here is somewhat simple. Had short sellers at the end of 2019 known how the next three-plus years would play out, every single one would have tripled their position.

In 2019, Trupanion generated Adjusted EBITDA of $10.7 million. The company then enjoyed a massive boom in pet ownership worldwide driven by the pandemic. Yet after Q1 2023, the trailing four-quarter figure was negative. Tangible book value admittedly has roughly doubled, but TRUP still trades at almost 4x the figure.

After the plunge, that fundamental case needs a bit of buttressing. Trupanion is still growing its top line, with revenue up 28% year-over-year in Q1. Management is attributing the weak bottom-line performance to veterinary inflation, which ran to 15% year-over-year in Q1, three percentage points worse than the company’s already-high expectation. That inflation should abate at some point, while President Margi Tooth argued on the Q1 conference call that inflation would drive adoption, since many potential customers didn’t have the savings to cover unexpected customer bills.

But there is an intriguing qualitative case here as well. Trupanion faces a significant “adverse selection” problem, in which owners of older and sicker (read: more expensive for the insurer) pets are less likely to defect. Both an inflationary environment (in which consumers are penny-pinching) and the simple ageing of the kittens and puppies acquired during the pandemic can amplify this problem. Trupanion management itself is pointing to coming price increases as a way to pass along inflation, but that in turn seems likely to increase churn.

Yet over the past four quarters, Trupanion has spent an average of $500-plus to acquire each pet in its subscription business. Higher churn means lower lifetime value, and with a medical loss ratio above 70% Trupanion needs customers to stay on for several years to drive profit growth from here.

For many of the speculative stocks we’re discussing here, one core question is whether the business model is actually viable in a normalized interest rate environment. (Carvana is a perfect example of this.) Trupanion in fact looks like it faces that very same question, particularly because unlike traditional insurers the company doesn’t get a benefit from higher rates. An awful lot of savvy shorts are betting that the answer here is ‘no’.

Affirm Sums It Up

“Buy now, pay later” provider Affirm encapsulates so many of the trends we’ve discussed to this point. AFRM stock has plunged from the peak (when it incredibly had a market cap of $46 billion), dropping a bit over 90%.

It saw a crazy rally earlier this month, gaining 16% (and nearly $800 million in market cap) in a single session the day after announcing a partnership with Amazon in which Affirm would be made available to merchants using Amazon Pay. Those gains were part of a 70% rally from early May lows.

Yet Affirm still has a market cap just shy of $5 billion — and remains unprofitable even on an adjusted basis. Operating margins are guided to negative 5.9 to negative 7.0 percent in fiscal 2023 (ending June) — but that excludes stock-based compensation tracking toward 30% of revenue this year, along with further share-based payments (such as the expense related to warrants held by Amazon as part of previous agreements).

Fundamentally, this looks like a slam-dunk short. And, qualitatively, again there’s a real question as to whether Affirm’s model works in a normalized interest rate environment. The company’s long-term 0% APR product is far and away its most profitable5 — but has become much more expensive over the past year.

The company’s funding costs have risen as well, leading the company to keep more loans on its own balance sheet. And while delinquency rates admittedly look solid, as we’ve noted repeatedly the U.S. consumer is much stronger than expected. The pending restart of student loan payments may provide near-term pressure on credit losses — pressure the current margin structure simply can’t handle.

This probably isn’t quite a short to zero trade. Affirm’s 2026 convertible notes yield a bit under 10%, suggesting relatively minimal odds of a zero over the next three-plus years6. There’s a world in which a slimmed-down Affirm becomes a niche business. Subprime lender Enova International, which has actually been rather successful since being spun from Cash America in 2014, has a market cap of about $1.65 billion, one-third that of Affirm.

Still, this is a short that seems to make some sense, even if it’s a short that hasn’t worked out over the past seven weeks. If investors flee speculative names, AFRM will likely be at the top of the list.

As of this writing, Vince Martin has no positions in any securities mentioned.

Stocks mentioned: AI 0.00%↑, ALLO 0.00%↑, AMC 0.00%↑, AMZN 0.00%↑, APE 0.00%↑, BBAI 0.00%↑, BLNK 0.00%↑, BTBT 0.00%↑, BYND 0.00%↑, CIFR 0.00%↑, CVNA 0.00%↑, ENVA 0.00%↑, EVA 0.00%↑, FATE 0.00%↑, NKLA 0.00%↑, NVAX 0.00%↑, NVDA 0.00%↑, PACW 0.00%↑, PLUG 0.00%↑, SYM 0.00%↑, TRUP 0.00%↑, ZIM 0.00%↑

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

For what it’s worth, we see it differently.

Congratulations to Beyond Meat for making both iterations.

To be clear, that’s not a brag; it’s not like we went out and shorted all those names.

The epitome of adding insult to injury.

A modeling presentation this month suggests merchant fee rates of 11-12% for long-term 0% APR loans, and under 2% for loans with a traditional interest rate.

The notes convert at $216 per share, against Wednesday’s close of $15.50, so there is obviously exceptionally little value in the equity portion.