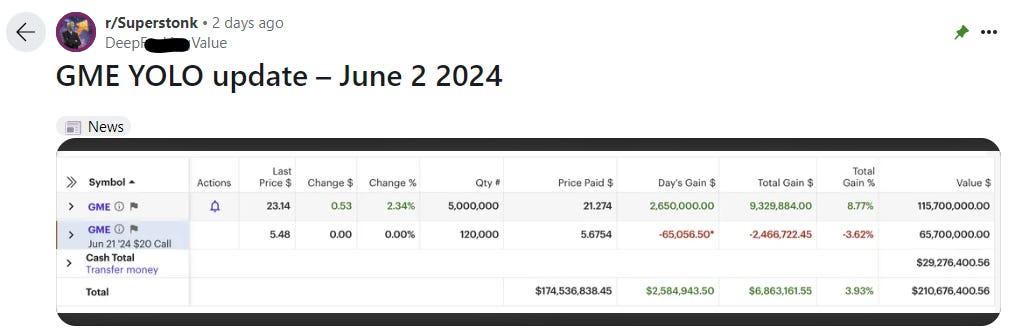

On Sunday evening, a Reddit account with the handle DeepF******Value posted a screenshot:

source: Reddit

The account seemingly belongs to Keith Gill, a former middle manager at an insurance company who became an apparent multi-millionaire thanks to the epic 2020-2021 run in GameStop. The same evening, Gill’s Twitter account posted the reverse card from the game Uno.

On Monday morning, GME opened up 74%. Shares have faded from those highs, but the stock has still moved, with two-day gains of 14.5%. That’s enough for Gill’s position — as represented in the Reddit post — to gain about $48 million in value1.

The unusual nature of Gill’s posts provides a window into a long-running debate over what kind of trading is legal and what’s not. The implications are useful for investors to understand and they highlight other important concepts — including the possibility of following insiders into (or out of) trades.

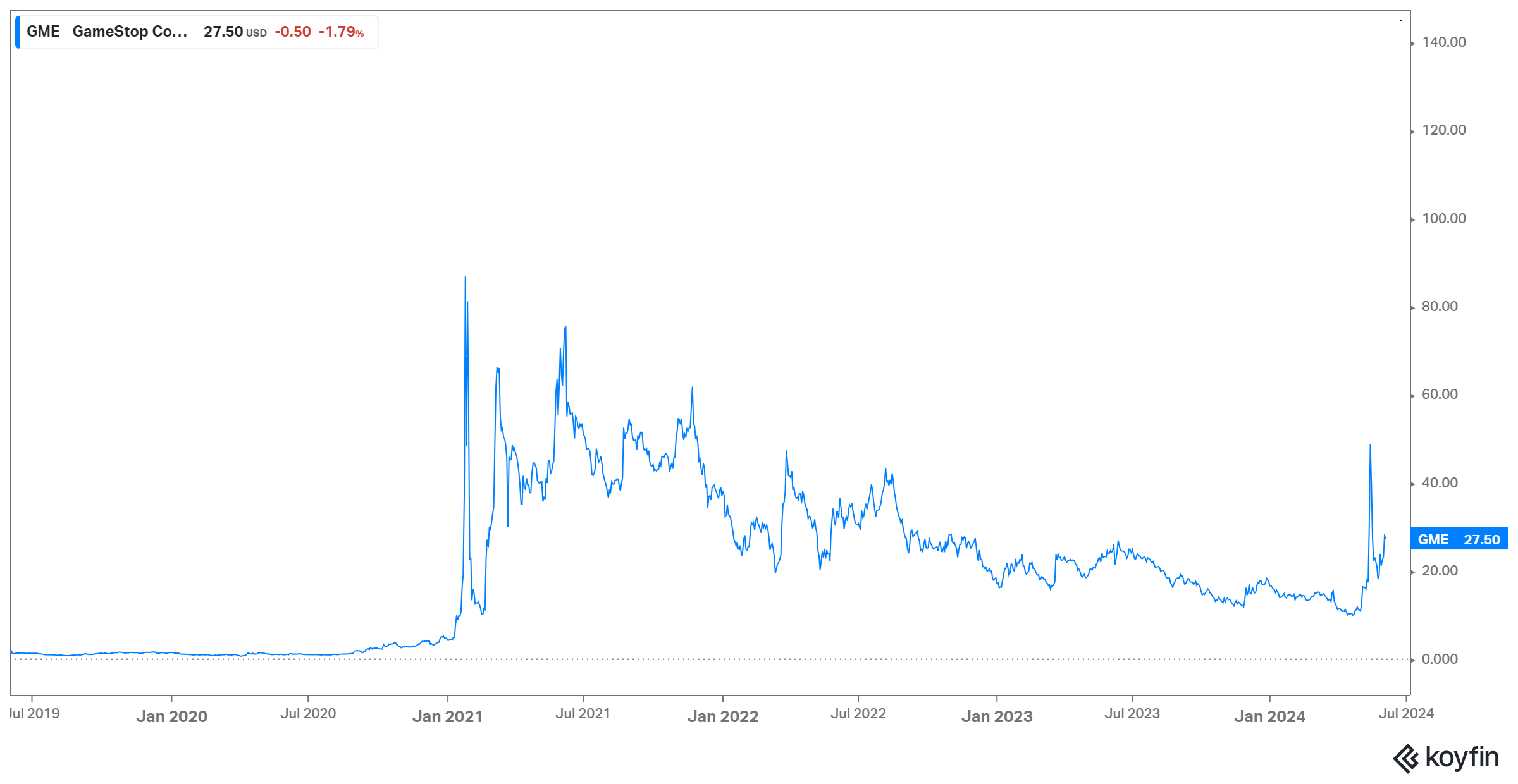

GameStop five-year chart; source: Koyfin.com

Is Keith Gill Committing Insider Trading?

Gill’s trade does look questionable from a number of angles, not least from the perspective of regulators. Indeed, the Massachusetts Secretary of State has confirmed an investigation into the trades. A leak from Morgan Stanley unit E*Trade suggests the broker is considering dropping Gill as a client owing to concerns about manipulation.

What does seem certain is that Gill is not committing insider trading. Despite that, the trade and his standing with GameStop actually provides an interesting structure through which to view cases where insider trading laws do apply.

(Disclaimer: The author has no legal training and nothing in this post should be relied on as legal advice.)

It’s worth noting first that Gill is not an insider: he’s not an officer or director of GameStop, nor is he a 10% shareholder. Even if the June options were exercised, which is the most likely outcome if they stay above their $20 strike price, he would still own less than 7% of the company.

Exercising an option means putting into effect the right to buy or sell the underlying security. After all, that is what an option is: it’s the right to buy or sell a stock at a specified price on or before the expiration date. To do this, you simply tell your broker that you wish to exercise the option. The reason Gill would likely exercise just ahead of expiration is that he probably has more liquidity in selling the stock acquired over time than in trying to sell 120,000 (!) call options within two weeks. Volume at that strike on Tuesday was less than 6,000; it simply will be hard to find that many buyers, even given the frenzied trade in GME options.

It’s possible (though unlikely) that Gill is part of a group that could, in theory, breach the 10% threshold. There’s been some speculation that Gill must be backed by someone, given that the Reddit screenshot shows an investment of $175 million, and that exercising the calls would require an incremental $240 million.

But even if Gill were an insider, his trade likely wouldn’t violate U.S. regulations. Insiders cannot trade on material non-public information (MNPI), but U.S. insider trading laws also require that an insider have a fiduciary duty to the company itself.

It’s possible, perhaps, to argue that Gill had material non-public information when he made the trade, knowing that his plans would stoke a social media fire that would send the stock higher. The catch in terms of the law is that Gill has no responsibility to or agreement with GameStop itself not to trade on that information. As the excellent Bloomberg columnist Matt Levine (himself a former securities lawyer) argued recently:

Insider trading, I like to say, is not about fairness: It’s about theft. In the US, most of the time, it is illegal to trade on inside information about a company not because that’s unfair to everyone else who doesn’t have the information, but because you have some duty to somebody else not to misuse their information.

Notably, the rules are different elsewhere. In Europe, as law firm Quinn Emanuel Urquhart & Sullivan has put it, insider trading regulation “is fundamentally underpinned by a notion of information parity and fairness across all market participants. [emphasis in original]”.

But in the U.S., the responsibility to the organization matters. It’s why Gill can trade on his information. It’s why Berkshire Hathaway can disclose its purchases after making them, even though the very fact the company is buying a stock likely makes it rise. (For instance, last month Chubb CB 0.00%↑ jumped 7% when Berkshire disclosed it had amassed a $6.7 billion investment over the preceding months.)

Of course, that applies to short sellers as well: the likes of Hindenburg Research can short a stock before they attack it publicly. Again, they have no responsibility to the company to protect non-public material information, such as the fact that a company’s trucks were rolled down a hill instead of propelled by an engine.

The Patchwork Of Insider Trading Law

What’s notable about the U.S. regime is that there isn’t actually a specific law against insider trading. At the federal level, the crime is prosecuted under Rule 10b-5 of the Securities and Exchange Act of 1934. But Rule 10b-5 covers securities fraud more broadly. What has come to be defined as insider trading has developed not from Congressional dictates, but largely from individual cases.

Those cases can be quite fascinating (Levine is constantly referencing the more interesting ones). Just in April, an executive at Medivation was convicted in a relatively novel case covering so-called “shadow trading”. The executive discovered that his company was about to be acquired by Pfizer PFE 0.00%↑ and bought call options on shares of another biotech, Incyte INCY 0.00%↑. He rightly assumed that the Medivation announcement would spike INCY stock; the trade made about $120,000. The SEC won the trial at jury, even while the agency acknowledged that there was no precedent for shadow trading to be considered a crime.

Other cases often revolve around whether a ‘tip’ from an insider is illegal. For decades, courts have wobbled over whether a “personal benefit” — in the most blatant example, a cash payment or profit-sharing agreement between the source of the information and the trader — is required for an insider trading conviction. What has been established is that the duty of an insider to protect information ‘travels’, so to speak, to close confidants. In February, a Houston man pleaded guilty to insider trading after overhearing his wife discuss a pending merger as she worked from home.

So while the broad sense of illegal insider trading has been established, there are continuing cases that define the boundaries of the crime: who is or is not an acceptable ‘tippee’; what actually constitutes MNPI; whether the so-called “mosaic theory”, in which a trader combines MNPI with more standard, acceptable research, should apply.

Overall, the importance of duty to the corporation remains paramount — and that focus has some logic. It’s good for the equity market if MNPI surfaces. It makes prices more accurate, which in turn helps direct capital formation across the economy. The debate, as seen in the differences between the American and European perspectives, might be how that information becomes public, and who profits in the process.

A Focus On Disclosure

Of course, insiders do trade in their own company’s stock and not all insider trading is illegal. In fact, most of it follows very basic rules. In the U.S. regime, insider trading regulation focuses on disclosure.

Any insider who buys or sells shares must disclose the trade in a Form 4, which must be filed within two business days. In addition, investors who accumulate a stake over 5% have to disclose that stake within five business days (that period was shortened last year from the previous ten business days). There are also periods in which insiders can’t buy, specifically when they are in possession on MNPI (think, for instance, the day before a quarterly earnings release, when executives know the results but the market does not).

Notably, those disclosures come after the trade is made — and those disclosures alone can move the stock. When Tesla CEO Elon Musk purchased shares of Twitter in 2022, the disclosure of his ownership — a disclosure which almost certainly was too late, violating regulations in the process — sent Twitter shares up 27% in three days.

As with other cases — think Berkshire or Hindenburg — this does seem potentially unfair, since Musk was able to buy Twitter at ~$37 with the knowledge that his purchases likely would move the stock higher2. But, again, insider trading regulation in the U.S. is not about fairness.

Some investors do put a great deal of emphasis on what is disclosed, particularly around insider buying. The old saw is that insiders can sell for many reasons: portfolio diversification, estate planning, or to raise cash for major purchases3. But insiders only buy for one reason: because they believe the stock is cheap.

Academic research suggests that, as a whole, insider trades are a reliable signal in both directions. Obviously, that does not mean every trade is a helpful signal — executives have their own biases and motivations which can influence decisions — but insider buying is an important vote of confidence in the stock. That appears particularly true during so-called “cluster buying”, in which multiple executives purchase stock at the same time.

And so there is an inherent logic to how legal insider trading is structured in the U.S. Insiders are rewarded: they generally get to buy at a price that doesn’t reflect all of the information they have. That in turn means, on average, those insiders receive immediate returns when that information does become public — even if that information is simply the disclosure of ownership by Berkshire, the building of a stake by an activist, or multiple, aggressive, buys by executives.

But it does appear that disclosure is quick enough that non-privileged investors can still profit off the signals provided. Even when understood after the fact, insider moves still matter.

As of this writing, Vince Martin has no positions in any securities mentioned.

Disclaimer: The information in this newsletter is not and should not be construed as investment advice. Overlooked Alpha is for information, entertainment purposes only. Contributors are not registered financial advisors and do not purport to tell or recommend which securities customers should buy or sell for themselves. We strive to provide accurate analysis but mistakes and errors do occur. No warranty is made to the accuracy, completeness or correctness of the information provided. The information in the publication may become outdated and there is no obligation to update any such information. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Contributors may hold or acquire securities covered in this publication, and may purchase or sell such securities at any time, including security positions that are inconsistent or contrary to positions mentioned in this publication, all without prior notice to any of the subscribers to this publication. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

We’re using the $8.10 midpoint of the bid/ask for the calls ($8.05/$8.15) as the current value of those options. They’ve added $262 per contract, or about $31.4 million, while the stock position has appreciated by $16.8 million.

Of course, Musk eventually acquired Twitter for $54.20 per share. The Washington Post estimated Musk saved about $156 million by buying before his stake was disclosed.

In April, Jefferies JEF 0.00%↑ CEO Rich Handler sold $65 million in stock because he wanted to buy a yacht.